American Express has refreshed its benefits for the U.S. Business Gold Card. The Amex U.S. Business Gold amplified benefits include new spending categories, statement credits, and a new design option. In addition, cardholders get access to useful tools for small business owners and entrepreneurs. Here’s what you need to know.

Amex Business Gold Card Refresh – New Categories, Statement Credits, and Design

The newly refreshed U.S. American Express Business Gold Card holds the value cardholders seek. According to an American Express survey, 86% of small businesses surveyed expressed they find the most value in flexibility, convenience, or a wide array of benefits. The recently added enhanced benefits check off every box for the most sought-out business credit card qualities.

“The refreshed Business Gold Card helps our Card Members spend more time on what’s important: running their business,” said Anna Marrs, Group President of Global Commercial Services and Credit & Fraud Risk at American Express. “Whether they’re making purchases for business needs like advertising, wireless bills, technology expenses, or on office supplies, booking travel, or dining with clients, the refreshed Business Gold Card will help small businesses unlock value.”

Earn Rewards with Versatility for Your Business Spending

With the U.S. American Express Business Gold Card, small business owners can earn 4X Membership Rewards® points for necessary business spending. Part of the reward enhancement includes two new reward categories. In addition to earning 4X Membership Rewards points on advertising, gas station purchases, and dining, cardholders can now earn maximum rewards for three new categories.

The new reward categories include U.S. purchases made from electronic goods retailers and software and cloud system providers. Cardholders can also earn 4X Membership Rewards points on wireless telephone service charges from a wireless service provider in the U.S. The third new category is a transit category for travel via trains, taxicabs, rideshare services, ferries, tolls, parking, buses, and subways. All other eligible items will earn 1x point.

(NEW) U.S. purchases made from electronic goods retailers and software & cloud system providers

(NEW) Monthly wireless telephone service charges made directly from a wireless telephone service provider in the U.S.

(NEW) Transit purchases including trains, taxicabs, rideshare services, ferries, tolls, parking, buses, and subways

Purchases at U.S. media providers for advertising in select media (online, TV, radio)

U.S. purchases at gas stations

U.S. purchases at restaurants, including takeout and delivery

Statement Credits and More!

Earning reward points for additional business spending is exciting. However, there are more benefits to be thrilled about, such as the two new statement credits. U.S. Business Gold Card members can access. Cardholders get a $240 Flexible Business Credit, which earns them $20 in statement credit each month for purchases at FedEx, Grubhub, and Office Supply Stores.

Additionally, card members can take advantage of the new Walmart+ membership credit, valued at $155 a year. Members will receive a monthly statement credit to cover the Walmart+ subscription. A Walmart+ membership has many benefits. Such as cash back on travel, free Walmart grocery delivery, free shipping, gas savings, video streaming with Paramount+, and more.

Furthermore, there is a new way to earn points for travel. When cardmembers make an eligible purchase through AmexTravel.com, they will earn 3X Membership Rewards points. So, if your small business requires lots of travel, this would be a great way to rack up points. Moreover, Amex has added the popular rose gold design to the mix. Cardholders can opt for the gold card or the rose gold color.

Valuable Protection

The Amex U.S. Business Gold Card has additional existing features and tools for small business owners, including built-in digital payment services, cashflow tools, and more. Part of the new set of amplified benefits includes cell phone protection, which is the equivalent of cell phone insurance. Cardholders can get reimbursed for repairs or replacement costs due to damage or theft. The maximum reimbursement is $800. Terms apply.

About American Express

American Express is a global integrated payments company, that provides customers access to products, insights, and experiences that enrich lives and build business success.

Do you have a rewards credit card that earns bonus points (or cash back rewards) on streaming services? Figuring out which services qualify can be confusing – but no more! Here is everything you need to know about streaming services and credit cards, including what banks/ issuers allow what streaming servcies:

This post may contain links from partner offers, and we may receive compensation when you click on links to these offers. Please see our advertiser and editorial disclosures above for more information. Citi is an advertising partner.

How Do Banks Classify Purchases?

Amazon Music

Fubo TV

Luminary

Paramount+

Spotify

Apple TV/ Music

HBO Max

MLB.tv

Peacock

Sticher

Audible

Standalone HBO

NBA League Pass

Prime Video

Tidal

DirecTV Stream

Hulu

Netflix

Showtime

YouTube Premium

Disney+

iHeartRadio

NHL.tv

Sling TV

YouTube Music

ESPN+

Kindle Unlimited

Pandora

SiriusXM

YouTube TV

Apple TV/ Music

FuboTV

SiriusXM

Bandcamp

HBO Now

Sling TV

DirecTV

Hulu

Spotify

Disney+

Netflix

Starz

ESPN+

Peacock

Tidal

Apple Music

HBO Max

Showtime

YouTube TV

Apple TV

Hulu

SiriusXM

Vudu

Disney+

Netflix

Sling

ESPN+

Paramount+

Spotify

FuboTV

Peacock

YouTube Premium

Amazon Music

Fubo TV

MLB.tv

Prime Video

Apple Music

HBO Max

NBA League Pass

Showtime

Apple TV+

YouTube (Music/TV)

Netflix

Sling TV

Audible

Hulu

NHL.tv

SiriusXM

DirecTV Stream

iHeartRadio

Pandora

Spotify

Disney+

Kindle Unlimited

Paramount+

Sticher

ESPN+

Luminary

Peacock

TIDAL

Amazon Music

DirecTV Stream

Pandora

Spotify

Amazon Prime Video

FUBO

Paramount Plus

Starz

AMC+

Google Play

Peacock

Vudu

Apple Music

HBO Max

Showtime

YouTube Music

Apple TV

iHeartRadio

SiriusXM

YouTube Premium

Audible

MLB.TV

Sling TV

YouTube TV

Disney+

Vudu

Google Play Music

FandangoNOW

YouTube Premium

Pandora

Hulu

Amazon Music

SiriusXM

Netflix

Apple Music

Slacker Radio

Sling TV

YouTube Music

Spotify

Apple Music

Apple News

Apple TV

Amazon Music Unlimited

Audible

Disney+

ESPN+

fuboTV

HBO Now

Headspace

Hulu

Kindle Unlimited

Netflix

NHL.tv

Pandora

Prime Video

Sirius XM Radio

Spotify Premium

Many rewards credit cards offer enhanced earnings in select categories. These categories are defined by what is known as an MCC – a Merchant Category Code.

A merchant category code is a four-digit number used to classify a business by the type of goods or services it provides. An MCC is a denomination that all merchants need in order to operate, whether they provide goods or services if they accept credit cards in exchange for their products.

This code can denote anything from “Eating Places” to “Drug Stores and Pharmacies,” “Fast Food Restaurants” to “Sporting Goods Stores.” The MCC is assigned to a business by the credit card processing networks when the business in question begins to accept credit cards as a form of payment and is often used by card issuers to classify the types of purchases cardholders make.

What Counts as a Streaming Service?

According to PC Magazine, a streaming service is “an online provider of entertainment (music, movies, etc.) that delivers the content via an Internet connection to the subscriber’s computer, TV, or mobile device.” Netflix, Hulu, Spotify, and Apple Music are high-profile examples of streaming services used by millions of Americans.

Many streaming platforms qualify as a “streaming service” through all banks (think Netflix, Hulu, Apple Music, etc.), while others are only allowed by select issuers.

Here is how each of the major credit card issuers classifies a streaming service:

American Express

American Express provides a generous selection of eligible streaming services, including live TV, music, radio, and more:

Amazon Music

Fubo TV

Luminary

Paramount+

Spotify

Apple TV/ Music

HBO Max

MLB.tv

Peacock

Sticher

Audible

Standalone HBO

NBA League Pass

Prime Video

Tidal

DirecTV Stream

Hulu

Netflix

Showtime

YouTube Premium

Disney+

iHeartRadio

NHL.tv

Sling TV

YouTube Music

ESPN+

Kindle Unlimited

Pandora

SiriusXM

YouTube TV

Some American Express personal cards come with statement credits for streaming and other digital entertainment purchases. The Platinum Card from American Express, for example, provides up to $240 annual digital entertainment statement credit for select providers ($20 monthly statement credits).

Citi

Citibank also provides a helpful list of the streaming services that count towards the 5% back categories with the Citi Custom Cash℠ Card. Those 5% back categories include fitness clubs, travel (including select local transit), gas, groceries, and yes, streaming. Keep in mind that the 5% bonus categories are limited to $500 spent every billing period, and any rewards earned after that threshold will be 1% back. All other purchases with the card earn unlimited 1% cash back, with no caps on that earning.

Here is the list of eligible streaming services according to Citi:

Amazon Music

Fubo TV

MLB.tv

Prime Video

Apple Music

HBO Max

NBA League Pass

Showtime

Apple TV+

YouTube (Music/TV)

Netflix

Sling TV

Audible

Hulu

NHL.tv

SiriusXM

DirecTV Stream

iHeartRadio

Pandora

Spotify

Disney+

Kindle Unlimited

Paramount+

Sticher

ESPN+

Luminary

Peacock

TIDAL

For those seeking a credit card that offers unlimited rewards, a card like the Citi® Double Cash Card may make more sense. Every purchase with the card earns 2% back in total. This 2% back works out as follows: 1% back when you make an eligible purchase with the card, and an additional 1% back when you pay off the corresponding balance. There is no limit to the amount of cash back earned.

Chase

Chase has a robust selection of credit cards that provide everyday value, with streaming services being one of the most popular categories. Select Chase cards, such as the Sapphire Preferred, earn impressive rewards on streaming (3X in the case of the Preferred).

Here is the current list of eligible streaming services for JP Morgan Chase:

Apple Music

HBO Max

Showtime

YouTube TV

Apple TV

Hulu

SiriusXM

Vudu

Disney+

Netflix

Sling

ESPN+

Paramount+

Spotify

FuboTV

Peacock

YouTube Premium

Special, Limited-Time streaming Bonus

Chase often provides special savings for select cardmembers, with the bank’s proprietary Freedom credit cards often enjoying significant value through these promotions. For example, through June 30, 2022, Chase Freedom and Freedom Flex cardmembers can receive 5% cash back on Amazon.com and Select Streaming Services purchases.

Keep in mind that only subscription services paid for with the listed selected merchants will quality for this offer: Disney+, Hulu, ESPN+, Netflix, Sling, Vudu, Fubo TV, Apple Music, Sirius XM, Pandora, Spotify, YouTube TV, HBO Max, Paramount+, Peacock, or Showtime.

Like Chase, Citi, and Amex, Capital One also features credit cards that are ideal for streaming. The bank’s Savor line of credit cards are excellent at this purpose, providing up to 4% cash back on eligible streaming subscriptions.

Capital One offers several versions of the Savor range, including a no annual fee version (the SavorOne, which earns 3% back on streaming) and the student version (also 3% back on streaming).

Here is the list of Capital One’s eligible streaming services:

Apple TV/ Music

FuboTV

SiriusXM

Bandcamp

HBO Now

Sling TV

DirecTV

Hulu

Spotify

Disney+

Netflix

Starz

ESPN+

Peacock

Tidal

Keep in mind that Some services, such as Prime Video, AT&T TV and Verizon FIOS On Demand, are excluded, as well as audiobook subscription services and fitness programming.

U.S. Bank

U.S. Bank offers streaming services as a bonus category on several credit cards, with the most prominent being the U.S. Bank Cash+® Visa Signature®. That card earns 5% back on two select categories you choose, 2% back on one “everyday” category a user selects, and 1% back on all other purchases.

Other cards that offer streaming points are the full line-up of the Altitude credit cards:

Altitude Reserve: 3X points on mobile wallet purchases (not streaming, but a great way to get around the issue)

Altitude Go: 2X points on streaming, plus a $15 annual streaming statement credit

Here is what U.S. Bank classifies as a streaming service:

Disney+

Vudu

Google Play Music

FandangoNOW

YouTube Premium

Pandora

Hulu

Amazon Music

SiriusXM

Netflix

Apple Music

Slacker Radio

Sling TV

YouTube Music

Spotify

Are There Other Options for Earning Rewards on Streaming with Your Credit Card?

While the above-mentioned credit cards and issuers prioritize streaming services as a bonus category, there are other ways to improve your rewards earning when it comes to streaming. Unlimited cash back credit cards are a great way to maximize your savings – regardless of what you spend your money on.

Here is a quick list of some of the leading unlimited cash back credit cards:

Remember, this list of unlimited cash back credit cards is not exhaustive. There are dozens of other competitive offers from regional banks and credit unions.

Are you tired of overspending during the holiday season? Do you find it difficult to save money while still getting everything you need? Well, Chase has good news for you! With the holiday season fast approaching, Chase is looking to help save consumers money with new, lucrative Chase Freedom welcome offers on its popular Freedom Unlimited and Freedom Flex credit cards, including $200 back and additional 5% cash back categories.

Chase Adds New Welcome Bonuses for Freedom Credit Cards

Chase is looking to help its cardholders accelerate holiday rewards with a new welcome offer on its popular Freedom credit cards. Effective immediately, this new acquisition offer is really three bonuses in one, with new Chase Freedom Flex and Freedom Unlimited cardmembers earning a $200 bonus after spending $500 on purchases in the first three months from account opening. Plus, they’ll earn 5% cash back on combined gas station and grocery store purchases (excluding Target and Walmart) at a cap of up to $12,000 spent in the first year of card membership.

With inflation continuing to impact Americans’ wallets, this new sign-up bonus is a welcome relief for anyone looking for a lucrative cash back credit card to boost their holiday season funds. This introductory offer is worth up to $800 in cash back on grocery and gas purchases.

Earn Everyday Rewards with Chase Freedom

Both cards also provide lucrative rewards every day. Chase Freedom Unlimited, for example, earns an unlimited 1.5% cash back or more on all purchases, like 3% on dining and drugstores and 5% on travel purchased through Chase. The Freedom Flex, Chase’s rotating cash back credit card, earns 5% cash back on up to $1,500 on combined purchases in bonus categories each quarter you activate. Plus, earn 5% cash back on travel purchased through Chase, 3% on dining, including takeout and drugstores, and 1% on all other purchases.

2023 Chase Freedom Calendar

The Chase Freedom 5% Cash Back Calendar for 2023 is as follows:

Date

5% Cash Back Category

Q1

January - March 2024

Grocery stores (excluding Walmart), self-care and spa services, plus fitness and gym memberships

Q2

April - June 2024

Restaurants, hotels, and Amazon.com and Whole Foods purchases

Q3

July - September 2024

Gas, EV charging, select live entertainment, and movie theatres

Q4

October - December 2024

PayPal, McDonald’s, pet shops and veterinary services, plus select charities

For Q4 2023, eligible Chase Freedom cardmembers earn 5% back on the first $1,500 on combined purchases at wholesale clubs, with select charities, or by using their card through PayPal. As always, there are caveats and fine print with these bonus categories, explained below:

Category

Explanation

Merchants in this category operate warehouse-style retail stores, sell in bulk, and concentrate on price appeal. These merchants sell a full range of household goods and merchandise, groceries, furniture, electronics, appliances, and auto supplies. These merchants may or may not have membership requirements. Gas, fuel, wholesale specialty service purchases such as travel, insurance, cell phone and home improvement will not qualify in this category. Delivery service merchants will be included if they classify as a wholesale club merchant. Mastercard not accepted at Costco warehouses or at gas stations.

Purchases made using PayPal at merchants in the current 5% quarterly categories will be awarded a total of 5% Cash Back rewards. Payments made through the Xoom transfer service are not eligible for 5%. Must have/open a PayPal account. Please note, Person-to-Person (P2P) transactions made with your Chase Freedom card on PayPal may be prohibited or not eligible for 5%.

Eligible charities include the American Red Cross, Equal Justice Initiatives, Feeding America, Habitat for Humanity, International Medical Corps, International Rescue Committee, Leadership Conference Education Fund, NAACP Legal Defense and Educational Fund, National Urban League, Thurgood Marshall College Fund, United Negro College Fund, UNICEF USA, United Way, World Central Kitchen, GLSEN, Out and Equal, and Sage.

Lengthy 0% Introductory APR Periods

The Chase Freedom Unlimited and Freedom Flex cards also come with lengthy introductory APR periods. Qualified new cardmembers can enjoy a 0% intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR based on creditworthiness and the Prime Rate. Other notable features of the cards include no annual fee and rewards that don’t expire as long as the account is open. Here’s how the two cards compare:

Earn 5% on up to $1,500 on combined purchases in bonus categories each quarter you activate. Plus, earn 5% back on Chase travel, 3% on dining and drugstores, and 1% on everything else

Earn 5% back on Chase travel, 3% on dining and drugstores, and 1.5% on everything else

Intro APR

0% for 15 months on purchases and transfers

0% for 15 months on purchases and transfers

Payment Network

Mastercard

Visa

These new welcome offers are worth considering for anyone searching for a rewarding credit card. With a generous spending bonus and 5% cash back on gas and groceries for the first year, plus 0% intro APR – it’s a deal that’s hard to pass up.

We’re almost sure it wouldn’t be such a terrible thing if we could all save money on rent. Today, we share a few practical tips that can save money on your monthly housing, including strategies you can try for better rental rates.

Practical Tips to Save Money on Rent

According to Statista, as of March of 2022, rents increased across all U.S. states. In February of 2023, the average rent of a two-bedroom apartment was 1,320 U.S. dollars, up from 1,282 U.S. dollars the prior year. For the average American, rent accounts for their highest monthly expense.

In the world of personal finance, the general rule is that at max, 30% of your income should go towards rent. For example, if your monthly income is $4,000, according to the 30% rule, rent should be a maximum of $1,200. However, following the 30% rule does not apply to everyone’s financial situation and may not necessarily apply to every person due to outside factors like inflation or job wages.

Due to rents taking up a major chunk of income for the average American, the benefits of reducing rental expenses are sought after. It can free up additional cash to be used elsewhere for saving and investing or as expendable income for fun experiences like travel and dining. With that said, there are a few actions you can take to help you save money on rent.

Do Your Research and Make a Plan

Negotiating Rent With Your Potential Landlord

Cost-Saving Strategies

Be Flexible

Building Good Credit and Rental History

Explore Discounts and Incentives

Do Your Research and Make a Plan

Rent is nothing to gamble with. After all, it’s typically one of the largest expenses the average citizen may have. For this reason, research and planning are crucial when trying to save money on your rent. First and foremost, we recommend you determine your budget and financial goals.

Understanding where your finances stand plays a major role because it informs you how much money you can realistically spend on housing a.k.a. rent. Essentials like housing, transportation, food, health, and clothing are the things you need to survive in a modern society. Making a plan to distribute your income accordingly will help you keep an affordable lifestyle to enjoy life.

During your research and planning phase, take note of rental market trends and average prices in your area. The more informed you are on your finances and the rental market, the better your decision on where to live. For extra savings on rent, consider alternative housing options like having a roommate or opting for shared housing.

Negotiating Rent With Your Potential Landlord

If you don’t ask, the answer will always be no. Before approaching your potential landlord (or landlady), do your research. Gather information on comparable rental properties in the area, then politely bring your findings to your landlord and express a reasonable request to negotiate down your rent. During your negotiation, highlight your positive rental history and willingness to sign a longer lease to entice a lowered monthly rental rate. While this strategy is not a sure win, it’s still worth the try for possible savings on rent.

Tip💡Explore Discounts and Incentives

Look for move-in specials or promotional offers from landlords

Consider renting during off-peak seasons for potential discounts

Explore rental assistance programs or subsidies if applicable

Cost-Saving Strategies

If your current rent is on the rise, evaluate your space and downsize if possible. Maybe you opted for a two-bedroom apartment to use the extra space for guests, a home office, or a home gym. Spare bedrooms may be a luxury you can live without. Downsizing to a 1-bedroom apartment or loft might be lower on rent and can save you a couple of hundred dollars a month. Additionally, stay mindful of your energy consumption to help keep a low utility bill for extra savings.

Be Flexible

Be open to relocating. Rental costs vary depending on the neighborhood or town. Moving to a more affordable city can make a huge difference. Big cities and downtown skyrises with convenient amenities tend to come with a heavy monthly rent.

Relocating to a suburb can save you money. However, moving away is not for everyone due to factors like a permanent job location or child care. It’s worth considering if you have a remote job and if you don’t mind a major change to a different city, county, or state with lower rent markets.

Building Good Credit and Rental History

Lastly, build a good credit and rental history to ensure you always snatch up the best deal on a potential home for rent. A good credit history will show landlords you are reliable and responsible. To the same effect, a prime credit score also shows you’re trustworthy enough to make your monthly rental payments. Why not pay rent and build credit at the same time? With the Bilt Credit Card, it is possible.

With Bilt, you can pay your monthly rent and earn rewards. The Bilt card earns 1x points on rent payments, 2x points on travel, and 3x points on dining. Additionally, it features no annual fee and no foreign transaction fees. There are many ways to redeem points. For example, you can use your earned points towards rent or a future down payment. Other ways to redeem rewards include travel, statement credits, and more.

How Will You Save Money on Rent?

There are plenty of strategies to choose from to save money on rent. Remember, rent prices vary widely across states and cities and with some creative thinking and flexibility, you may come across affordable rents that won’t break the bank. Whether you choose to move away to a more affordable neighborhood or decide on getting a roommate, there are always ways to improve your situation with a little bit of sacrifice. You just have to think outside the box.

Amazon’s Prime Day is one of the most hotly-anticipated shopping events of the year. For 2023, the online shopping extravaganza takes place over two days in July – and also two extra days in October – giving savvy consumers even more time to snag a bargain. But what are the best credit cards for maximizing your savings on Prime Day 2023?

Amazon Prime Day is a multi-day event exclusively for Amazon Prime members. During the event, Amazon offers doorbuster deals on everything from televisions and appliances to home furnishings, clothing, and more.

Amazon’s flagship event already took place over the summer, but it will now run for two additional days this month and labeled as “Prime Big Deal Days”. The sales will from October 10 at 3 a.m. EDT to October 11, 2023. The event is open to Amazon Prime members in Austria, Australia, Belgium, Brazil, Canada, China, France, Germany, Italy, Japan, Luxembourg, Mexico, the Netherlands, Portugal, Singapore, Spain, the U.K., the U.S., and for the first time in Poland and Sweden.

Prime customers can shop products from top national brands and more third-party sellers than on last year’s Prime Day, including many small and medium-sized businesses. New deals – from fashion and electronics to toys and home goods – will go live throughout Prime Big Deal Days, offering savings on products across categories, including from Customers’ Most Loved, Internet Famous, and a selection of Climate Pledge Friendly products.

What are the Best Credit Cards for Amazon Prime Big Deal Days 2023?

Here are some of the top picks for credit cards to use on Prime Big Deal Days:

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

VisaProcessing Network

NoneAnnual Fee

Prime Visa

18.74% to 26.74% variableRegular Purchase APR

18.74% to 26.74% variableBalance Transfer APR

29.49% variable based on the Prime RateCash Advance APR

At a

Glance

The Prime Visa offers cardholders impressive rewards on all Amazon.com and Whole Foods purchases, as well as elevated cash back at gas stations, drug stores, restaurants, transit, commuting, and more.

Best Benefits

Rates & Fees

Why Should You Apply?

Instant Amazon.com gift card on approval

Earn 5% Back at Amazon.com and Whole Foods Market with an eligible Prime membership, plus 5% Back on purchases made through Chase Travel.

Earn 2% Back at restaurants, gas stations, and drugstores, plus 2% Back on local transit and commuting, including rideshare.

Earn 1% Back on all other purchases

No foreign transaction fees

No annual fee

Regular Purchase APR:

18.74% to 26.74% variable

Intro Balance Transfer APR:

N/A

Balance Transfer APR:

18.74% to 26.74% variable

Balance Transfer Transaction Fee:

Either $5 or 5% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.49% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Late Payment Penalty Fee:

Up to $39

Return Payment Penalty Fee:

Up to $39

Minimum Deposit Required:

N/A

You frequently shop at Amazon or Whole Foods

You have an existing Amazon Prime membership

You want a card with no foreign transaction fees and Visa concierge services for your travel plans

You want a flexible rewards program, including savings at gas stations dining

You want the excellent customer service Amazon is known for

The Amazon Prime Rewards Visa Signature® Card is seemingly designed for Prime Day and Prime Big Deal Days. The card earns up to 5% back at Amazon.com and Whole Foods, making it a great option for getting groceries shipped directly to your door via either Whole Foods or Amazon Fresh.

What makes the Prime Visa such a robust Prime Day and Big Deal Days credit card are the unique features it offers cardmembers, both new and old:

New cardmember welcome offer: New Prime members can get a $150 Amazon Gift Card instantly upon approval for Prime Visa.

6% back on Prime Day: Cardmembers earn unlimited 6% back on Prime Day at Amazon.com, Amazon Fresh, and Whole Foods Market with an eligible Prime membership (5% back year round). Plus, with daily rewards, earnings can be redeemed at Amazon.com or Chase as soon as the next day.

Extra rewards with No-Rush Shipping on Prime Day: Prime cardmembers can also earn an additional 1% back on eligible Amazon purchases with No-Rush Shipping (for a total of 6% back with an eligible Prime membership).

The card requires a Prime membership to maximize rewards. Having Prime, for instance, bumps up the cash back to 5% at Amazon and Whole Foods. No Prime membership means cardholders earn just 3% back at Wholefoods and Amazon – not great, but better than average.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

$0Annual Fee

Citi® Double Cash Card – 18 month BT offer

18.99% - 28.99% (Variable)Regular Purchase APR

18.99% - 28.99% (Variable)Balance Transfer APR

29.99% (Variable)Cash Advance APR

At a

Glance

The Citi® Double Cash Card is one of the most versatile cash back credit cards on the market today, thanks to impressive, flat-rate cash back, lucrative introductory 0% APR offers, and more. Cardholders earn 2% back on every eligible purchase: 1% back at the time of sale and an additional 1% back when they pay their statement balance. Cash back is redeemable for statement credits, direct deposits, checks, or converted as ThankYou® points.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases.

To earn cash back, pay at least the minimum due on time.

Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 18.99% - 28.99%, based on your creditworthiness.

Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Regular Purchase APR:

18.99% - 28.99% (Variable)

Intro Balance Transfer APR:

0% for 18 months on Balance Transfers

Balance Transfer APR:

18.99% - 28.99% (Variable)

Balance Transfer Transaction Fee:

3% of each transfer (minimum $5) completed within the first 4 months of account opening. A balance transfer fee of 5% of each transfer ($5 minimum) applies if completed after 4 months of account opening.

Cash Advance APR:

29.99% (Variable)

Cash Advance Transaction Fee:

5% of each cash advance; $10 minimum

Penalty APR:

Up to 29.99% (Variable)

Annual Fee:

$0

Foreign Transaction Fee:

3%

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $41

You prefer earning cash back at a flat rate rather than in rotating categories

You're looking to either consolidate existing balances or pay down a large purchase with no interest charges for an extended period of time

You like to have the flexibility of converting cash back into lucrative rewards points

You're considering a credit card without an annual fee

Prime Day has shifted its date over the years. Despite that, the sales event usually fell into the 5% bonus cash back category of at least one rotating cash back credit card – but not so this year. Unlimited cash back cards offer cash back at an elevated rate – typically between 1.5% and 2% back – on every eligible purchase.

The Citi® Double Cash Card earns a flat-rate 1% cash back on all eligible purchases – and another 1% back when the account holder pays off those purchases. Additionally, the card features no annual fee and a lengthy 18-month 0% intro APR offer for new accounts.

The lack of an annual fee, the prospect of 2% back, and the 0% introductory APR on balance transfers for the first 18 months make the Citi Double Cash Card the perfect everyday credit card for looking to save the Prime Day or hoping to pay down an existing card balance.

The Double Cash from Citi earns rewards as ThankYou Points. Cardmembers can opt for statement credits, gift cards, merchandise, or other award options or use their points to book travel through Citi ThankYou® Rewards.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

VisaProcessing Network

NoneAnnual Fee

Chase Freedom Unlimited®

18.24% to 27.74% VariableRegular Purchase APR

18.24% to 27.74% VariableBalance Transfer APR

28.49% VariableCash Advance APR

0% for 15 months from account opening dateIntro Purchase APR

At a

Glance

The Chase Freedom Unlimited® credit card is a reliable option for customers looking to pair an attractive cash back rewards program with generous introductory interest rates. Cardholders can redeem for cash, travel, and more.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn a $200 Bonus after you spend $500 on purchases in your first 3 months from account opening

Enjoy 5% cash back on travel purchased through Chase Travel℠, our premier rewards program that lets you redeem rewards for cash back, travel, gift cards and more; 3% cash back on drugstore purchases and dining at restaurants, including takeout and eligible delivery service, and 1.5% on all other purchases.

No minimum to redeem for cash back. You can use points to redeem for cash through an account statement credit or an electronic deposit into an eligible Chase account located in the United States!

Enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 18.24% - 27.74%.

No annual fee – You won't have to pay an annual fee for all the great features that come with your Freedom Unlimited® card

Keep tabs on your credit health, Chase Credit Journey helps you monitor your credit with free access to your latest score, alerts, and more.

Member FDIC

Intro Purchase APR:

0% for 15 months from account opening date

Regular Purchase APR:

18.24% to 27.74% Variable

Intro Balance Transfer APR:

0% for 15 months from account opening date

Balance Transfer APR:

18.24% to 27.74% Variable

Balance Transfer Transaction Fee:

Either $5 or 5% of the amount of each transfer, whichever is greater.

Cash Advance APR:

28.49% Variable

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each transaction, whichever is greater

Penalty APR:

Up to 29.99% Variable

Foreign Transaction Fee:

3% of the transaction amount in U.S. dollars

You are looking for a low-rate credit card to perform a balance transfer

You prefer straightforward rewards earnings rather than quarterly categories requiring activation

You'll make at least $500 in purchases in the first 90 days

The Chase Freedom Unlimited earns an unlimited 1.5% cash back on all purchases except for extra enhanced categories. The card also earns 3% back on bonus categories of dining and restaurant purchases, including take-out orders and deliveries through eligible delivery services like GrubHub and Uber Eats. That 3% back also applies to drugstore purchases.

For Prime Day, new cardmembers can enjoy 0% Intro APR for 15 months from account opening on purchases and balance transfers – perfect for paying off big purchases over time.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

American ExpressProcessing Network

$0 for the first year. Then $95Annual Fee

Blue Cash Preferred® Card from American Express

19.24% to 29.99% variable based on creditworthiness the Prime RateRegular Purchase APR

19.24% to 29.99% variable based on creditworthiness the Prime RateBalance Transfer APR

29.99% variable based on the Prime RateCash Advance APR

0% for 12 months from account opening dateIntro Purchase APR

At a

Glance

Through the Blue Cash Preferred® Card from American Express, you can earn sizable cash back rewards on purchases in common categories, including 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1%), 3% cash back at U.S. gas stations and select U.S. department stores, and 1% on all other purchases. You can also earn $300 back in the form of a statement credit after you make $3,000 in purchases using your new card in the first six months of the account being open.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn a $300 statement credit after you spend $3,000 in purchases on your new Card within the first 6 months.

$0 intro annual fee for the first year, then $95.

Buy Now, Pay Later: Enjoy $0 intro plan fees when you use Plan It® to split up large purchases into monthly installments. Pay $0 intro plan fees on plans created during the first 12 months from the date of account opening. Plans created after that will have a monthly plan fee up to 1.33% of each eligible purchase amount moved into a plan based on the plan duration, the APR that would otherwise apply to the purchase, and other factors.

Low Intro APR: 0% on purchases and balance transfers for 12 months from the date of account opening. After that, your APR will be a variable APR of 19.24% - 29.99%. Variable APRs will not exceed 29.99%.

6% Cash Back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%).

6% Cash Back on select U.S. streaming subscriptions.

3% Cash Back at U.S. gas stations and on transit (including taxis/rideshare, parking, tolls, trains, buses and more).

1% Cash Back on other purchases.

Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit

Get up to $120 in statement credits annually when you pay for an Equinox+ membership at equinoxplus.com with your Blue Cash Preferred® Card. That's $10 in statement credits each month. Enrollment required.

Thinking about getting The Disney Bundle which includes Disney+, Hulu, and ESPN+? Your decision made easy with $7/month back in the form of a statement credit after you spend $12.99 or more each month on an eligible subscription with your Blue Cash Preferred Card. Enrollment required.

Terms Apply.

Intro Purchase APR:

0% for 12 months from account opening date

Regular Purchase APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Intro Balance Transfer APR:

0% for 12 months from account opening date

Balance Transfer APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Balance Transfer Transaction Fee:

Either $5 or 3% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.99% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Penalty APR:

29.99% variable based on the Prime Rate

Annual Fee:

$0 for the first year. Then $95

Foreign Transaction Fee:

2.7% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $40

Return Payment Penalty Fee:

Up to $40

You budget for family spending and want a credit card that earns significant cash back

You'll spend a lot of money on groceries to take advantage 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1% after that)

You're excited at the prospect of earning 6% cash back with select streaming services

You want to capitalize on your commute with 3% cash back at U.S. gas stations (and select U.S. department stores)

You'll take advantage of 3% cash back on transit (taxis/rideshare, parking and tolls, trains, buses and more), and 1% on all other purchases

You're likely to make $3,000 in purchases within the first six months of the account opening to qualify for a one-time $300 statement credit

You cook at home often and commute to work and school regularly, or make use of public transit regularly

The Blue Cash Preferred® Card from American Express is an excellent option for Prime Day and Prime Big Deal Days 2023. Amazon offers a vast assortment of services, including groceries (Amazon Fresh / Whole Foods Market), music (Amazon Music Unlimited), and streaming (Amazon Prime Video).

The Blue Cash Preferred earns 6% back on streaming services and 6% back on U.S. groceries (up to $6,000 per year), making it an excellent option for anyone planning to stock up on provisions or maybe add a new premium channel to their Prime Video viewing lineup.

The Capital One® Savor® Cash Rewards Card is another great option at a similar price point (both cards feature a $95 annual fee). The Savor earns unlimited 4% back on streaming and groceries, making it a great choice for someone who wants the enhanced earning of the Preferred, but not the caps on earning it.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good / Fair

VisaProcessing Network

NoneAnnual Fee

Upgrade Cash Rewards Visa®

14.99%-29.99% variable based on creditworthiness and the Prime RateRegular Purchase APR

14.99% to 29.99%Balance Transfer APR

At a

Glance

The Upgrade Cash Rewards Visa® offers no fees, low rates, cash back, and credit lines from $500 to $25,000 in one unique package. The card provides consumers the flexibility and predictability to quickly pay down balances and get debt-free. The Upgrade credit card is one of the lowest regular APR credit cards on the market for those with excellent credit scores, putting it firmly on any list of the best balance transfer credit card deals – or any list of the best credit cards in the U.S.

Best Benefits

Rates & Fees

Why Should You Apply?

$200 bonus after opening a Rewards Checking Preferred account and making 3 debit card transactions*

1.5% unlimited cash back on every purchase

No annual fee

See if you qualify in seconds with no impact to your credit score

Combine the flexibility of a card with the predictability of a personal loan

Enjoy Visa Signature benefits, like Roadside Dispatch, Price Protection, Extended Warranty Protection, and more

Shop smarter with Upgrade Shopping! Get exclusive savings at stores, restaurants, and more

Contactless payments with Apple Pay® and Google Wallet™ bull; Mobile app to access your account anytime, anywhere

Use your card anywhere Visa is accepted

Relax knowing that you are protected in case of unauthorized transactions with Visa’s Zero Liability Policy

Regular Purchase APR:

14.99%-29.99% variable based on creditworthiness and the Prime Rate

Balance Transfer APR:

14.99% to 29.99%

Balance Transfer Transaction Fee:

Up to 5%

Foreign Transaction Fee:

Up to 3%

Late Payment Penalty Fee:

May apply

You struggle to pay off your credit card balances

You want a structured repayment plan

You can reliably pay off your statement balances to earn cash back for your purchases

The Upgrade Cash Rewards Visa® provides a great mix of unlimited cash back and an exceptional APR. That APR on purchases and balance transfers starts as low as 9% for applicants with excellent credit.

Instead of 0% APR Upgrade prioritizes a great rate along with a unique repayment plan that is more akin to a personal loan than a traditional credit card account. Cardholders pay off balances significantly faster with Upgrade versus other low APR credit cards. According to research from Upgrade, paying off a $10,000 balance takes just a few years with the Upgrade Visa, compared with other traditional credit cards that can take up to 20 years – or more.

Add to that great rate simplified cash back rewards, and you have the makings of an excellent low APR credit card. Even better, that 1.5% cash back applies to every purchase, making the Upgrade Cash Rewards Visa a versatile credit card suitable for Prime Day, Black Friday, Arbor Day – or any day.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

NoneAnnual Fee

BankAmericard® Credit Card

16.24% to 26.24% variable based on creditworthiness and Prime RateRegular Purchase APR

16.24% to 26.24% variable based on creditworthiness and Prime RateBalance Transfer APR

19.24% to 29.24% variable based on the Prime RateCash Advance APR

0% for 18 months from account opening dateIntro Purchase APR

At a

Glance

The BankAmericard Mastercard is the balance transfer card designed for those who want a special intro rate and little else. The card features 0% intro APR on purchases and balance transfers for the first 18 months. The card also boasts no penalty APR and no annual fee.

Best Benefits

Rates & Fees

Why Should You Apply?

No interest charges on purchases and balance transfers for the first 18 months from the date of account opening

No penalty APR for late payments

No annual fee

Access your FICO® Score for free

Intro Purchase APR:

0% for 18 months from account opening date

Regular Purchase APR:

16.24% to 26.24% variable based on creditworthiness and Prime Rate

Intro Balance Transfer APR:

0% for 18 months for any balance transfers made within 60 days from account opening date

Balance Transfer APR:

16.24% to 26.24% variable based on creditworthiness and Prime Rate

Balance Transfer Transaction Fee:

Either $10 or 3% of the amount of each transfer, whichever is greater

Cash Advance APR:

19.24% to 29.24% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each transaction, whichever is greater

Foreign Transaction Fee:

3% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $40

Return Payment Penalty Fee:

Up to $29

You plan to make a large purchase and use the card to pay off the balance over time

You have existing credit card balances to combine and pay down

You would think that the list of best credit cards for Prime Day would be exclusively rewards – but that’s not the case. After all, earning points is great, but being able to finance a big Prime Day purchase over 12, 15, or even 18 months interest-free should sound like a great deal to anyone. And that’s where the BankAmericard® from Bank of America comes in.

The BankAmericard offers two exceptional introductory periods: 0% intro APR for 21 months on purchases and balance transfers made within the first 60 days of account opening, with a highly competitive, low variable APR after that. That 21 months of interest-free financing on purchases is among the longest 0% APR periods for any card – and adding 21 months of 0% APR on transfers just sweetens the pot.

While the BankAmericard might not have many flashy features, like the Double Cash or Freedom Unlimited, it is a solid card for people who can appreciate no annual fee, no penalty APR, and no nonsense.

Looking to find the best credit cards for bad credit? The BestCards team has you covered with our guide to the top choices for rebuilding a damaged credit score.

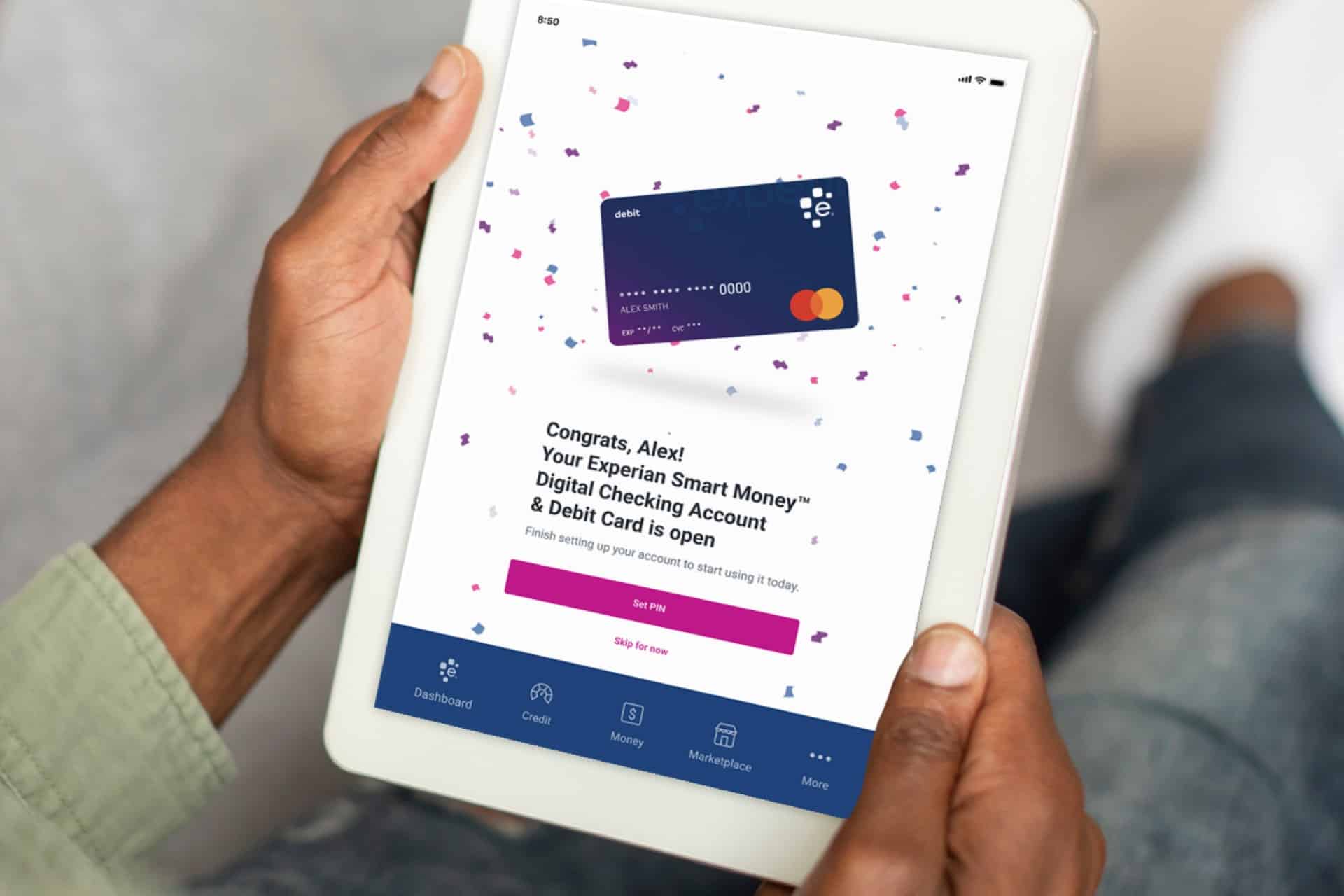

Experian has a new digital checking and debit card program for those looking to build credit. The new Experian Smart Money™ Digital Checking Account comes with Experian Boost built in, providing even more ways to give consumers credit for paying regular bills like utilities, rent, phone plans, and more.

Experian Launches New Debit Card and Checking Account

The Experian Smart Money™ debit card and checking account is designed by the credit experts at Experian, one of the leading consumer credit reporting agencies. Instead of operating like a charge card – where cardholders purchase with their debit card and then Experian automatically debits the purchase price and counts that as a card transaction – Experian Smart Money™ works by automatically linking with Experian Boost.

What is Experian Boost?

Experian Boost is a free tool designed to help consumers improve their FICO® Score with everyday expenses. The program lets customers link monthly utility bills and other recurring transactions and then reports positive credit actions, such as on-time payments, to the credit bureaus – thereby helping them build credit.

The program works for utility, telecom, rent, and certain streaming service payments. What’s more, Experian does not look for negative payment histories, and the boost benefits are immediate.

This regular reporting can help to quickly raise your credit score after a series of on-time payments. This benefit is often under-appreciated, as payment history is the biggest determining factor in calculating your credit score (35% of a FICO Score and 30% for VantageScore). According to Experian’s data, the average credit score increase from Experian Boost is around 19 points – with some users reporting more significant gains while others reporting little-to-no FICO Score movement.

One of the great features of the new Experian Smart Money™ debit card is the addition of a welcome bonus – something normally not seen with non-credit card products. New accounts receive a $50 bonus after setting up a direct deposit – a very easy reward to attain.

No Hidden Fees

The card contains no hidden fees of any kind. This means there are no account minimums or monthly maintenance fees. Some credit builder debit cards charge a monthly maintenance fee or a surcharge for access to credit-building features or elite rewards. Not so with Experian Smart Money, however.

Reload at Thousands of Merchants

Equally enjoyable is loading funds via cash at select retailers nationwide. Cash reloads are accepted through specified third-party money transfer services that participate in the Mastercard rePower Load Network, including Green Dot, MoneyGram, and Vanilla. Those wishing to deposit funds the traditional way can also do so, with users able to add money by transferring from another bank account or setting up direct deposit.

Other Card features

There’s more, too. Cardholders enjoy access to over 55,000+ no-fee ATMs worldwide. That feature is exceptional – as anyone who has spent hours on vacation looking for an overseas ATM that won’t charge an astronomical surcharge can tell you. The card is also FDIC-insured for up to $250,000 thanks to a partnership with Community Federal Savings Bank – the card’s issuer.

The Experian Smart Money™ debit card is a Mastercard debit product, meaning cardholders can also expect the following protections and benefits:

ID Theft Protection

Zero Fraud Liability

Mastercard Global Service customer support

Purchase Protection

Extended Warranty Protection

Mastercard Hotel Stay Guarantee

“We’ve Made it More Seamless”

“With Experian Boost and Experian Go, we enabled millions of people who pay bills regularly to leverage their positive payment history to build their credit profiles. Now, we’ve made it more seamless to have those positive payments reflected with the Experian Smart Money™ Digital Checking Account so more consumers can reach their fullest financial potential,” said Jeff Softley, Group President of Experian Consumer Services at Experian, in a press release. “We have been revolutionizing the way credit and everyday finances mingle, and this offering is a natural next step in how we are using our technology to provide consumers greater credit-building power and financial control.”

Experian Taps Travis Kelce for Assistance

To highlight the launch of the new Experian Smart Money Card, the reporting agency has joined up with two-time professional football champion Travis Kelce of the Kansas City Chiefs. This campaign seeks to generate awareness about the new Experian Smart Money™ Digital Checking Account and debit card. “When it comes to finances, it’s better to work smarter rather than harder,” said Kelce. “This is a great opportunity for me to spread the word about the resources available, like Experian’s new digital checking account to help fans become the champion of their finances.”

“The passion that fans have for Travis and football is a great way to think about your finances – we want consumers to have that same passion for their financial health,” adds Dacy Yee, Chief Marketing Officer, Experian Consumer Services at Experian. “Experian is here to help every consumer take control of their finances, and the excitement around football reaches a diversity of people from college students to seasoned professionals. This new digital checking account can help everyone along their financial journey, including building their credit strength.”

If you have bad credit, you may feel like there are limited options for obtaining new credit to help repair your credit score This confusing process is particularly problematic if you need to make a large purchase or are trying to rebuild your credit score. Fortunately, credit card options are available for individuals with bad credit, including “second chance” credit cards.

A “second chance” credit card is a special type of credit card designed specifically for anyone with a bad credit score. These credit cards help you rebuild your credit score by offering credit with lower limits and higher interest rates. These credit cards are called “second chance” because they give you a second chance to obtain credit after experiencing financial hardship or adverse financial events.

How Does a "Second Chance" Card Work?

“Second chance” credit cards work much like traditional credit cards. You apply for the credit card, and if approved, you receive a credit limit. You can use the credit card to make purchases like any other credit card. The most significant difference is that these credit cards often have higher interest rates and fees vs. traditional credit cards.

One of the benefits of a “second chance” credit card is that it can help you rebuild your credit score. Using your credit card responsibly by making on-time payments and keeping your balance low can help improve your credit score. However, misusing the card by making late payments or maxing out your credit limit can harm your credit score.

What are the Best "Second Chance" Credit Cards?

One of the biggest challenges consumers face when applying for a credit card is the credit check. While secured credit cards require a cash deposit to open, they aren’t always a guaranteed approval – which can deter many people from applying. Fortunately, there are several excellent secured cards that don’t require a credit check.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Poor / No Credit Required

VisaProcessing Network

$35Annual Fee

opensky® Secured Visa® Credit Card

23.89% (variable)Regular Purchase APR

23.89% (variable)Cash Advance APR

At a

Glance

The opensky® Secured Visa® is a secured credit card that offers requires a low minimum deposit and features no credit checks for approval. The card, issued by Capital Bank, provides an easy route to better credit by offering credit limits as low as $200, a moderate fixed-rate APR, and a reasonable $35 annual fee.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn up to 10% cash back on everyday purchases

No credit check required – 89% approval rate with zero credit risk to apply!

Boost your credit score fast—2 out of 3 opensky® cardholders see an average increase of 47 points after 6 months

Track your progress with free access to your FICO® score in our mobile app

Build your credit history with reporting to all three major credit bureaus: Experian, Equifax, and TransUnion

Seamless payments—add your card to Apple Pay, Google Pay, and Samsung Pay

Start with just $200—secure your credit line with a refundable deposit

Fast and easy application—apply in minutes with our mobile-first experience

Flexible payment options—pick a due date that works for you

More time to fund—spread your security deposit over 60 days with layaway

Join 1.6 million+ cardholders who have used opensky® to build better credit!

Regular Purchase APR:

23.89% (variable)

Cash Advance APR:

23.89% (variable)

Cash Advance Transaction Fee:

Either $6 or 5% of the amount of each cash advance, whichever is greater.

Annual Fee:

$35

Foreign Transaction Fee:

3% of each transaction in U.S. dollars

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $25

Minimum Deposit Required:

$200

You're struggling to get accepted for other secured credit cards

You don’t have a credit history

You have bad credit and want to improve your credit score

You have a large deposit and want a quick pick-me-up for their credit score

You want access to a useful knowledge base of credit information and resources

The OpenSky Visa is one of the best secured credit cards on the market – and it is just as good as a “second chance” card if you find yourself striking out elsewhere. One reason why is that OpenSky requires no credit check. The card application process is straightforward and takes just a few minutes. Decisions are equally quick, making the entire process fast and painless.

The OpenSky credit education hub offers a range of articles on building credit, making it a useful partner in building up your credit knowledge as your payments build up your credit score. These topics include how to receive a free copy of your credit score, how credit scores are calculated, tips on boosting credit, and other advice related to the OpenSky card.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Fair / Poor / No Credit Required

VisaProcessing Network

$25Annual Fee

Self Visa® Credit Card

27.49% (Variable)Regular Purchase APR

At a

Glance

The Self Visa® Credit Card is a secured credit card that pairs with an existing Self Credit Builder Account. The card has no formal approval process. Instead, hopeful consumers simply need to open a Self account and save over $100 to fund the secured Visa account.

Best Benefits

Rates & Fees

Why Should You Apply?

Apply Now: Intro No Annual Fee with the secured Self Visa® Credit Card^ • If you have an active Credit Builder Account, $100 or more in savings progress and satisfying income requirements you may be eligible to receive the secured Self Visa® Credit Card*, without a hard credit check. Criteria subject to change. • Build credit and savings at the same time. • Start with a Credit Builder Account* that reports monthly payments to all 3 major credit bureaus. • At the end of your plan, unlock the savings you built - minus interest and fees. • The secured Self Visa® Credit Card is accepted at millions of locations in the U.S. *Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., First Century Bank, N.A., each Member FDIC. Subject to credit approval. The secured Self Visa® Credit Card is issued by Lead Bank or First Century Bank, N.A., each Member FDIC. See Self.inc for details. Subject to ID Verification. Individual borrowers must be a U.S. citizen or permanent resident and at least 18 years old. Valid bank account and Social Security Number are required. All loans are subject to consumer report review and approval. The Secured Self Visa® Credit Card requires an active Self Credit Builder Account and qualification based on other eligibility criteria including income & expense requirements. Criteria subject to change. ^$0 annual fee for the first year only, $25 annual fee thereafter. Variable APR of 28.24%. Offer valid for new customers only.

Regular Purchase APR:

27.49% (Variable)

Annual Fee:

$25

Late Payment Penalty Fee:

Up to $15

Return Payment Penalty Fee:

Up to $15

You're serious about raising your credit score

You already have a Self Credit Builder Account

You don’t mind the card's $25 annual fee

You plan to pay your card balance in full every month

Building credit is difficult without the correct tools. Fortunately, the Self Secured Visa makes the practice much easier. The Self Visa Credit Card is a secured card designed to help build credit – fast, with no credit check required.

Because Self is a credit builder startup, the process involves a potential applicant getting their hands dirty with the company and growing their credit portfolio. This process begins with opening a Self Credit Builder Account. Self’s Credit Builder Account is a unique loan product ideal for you if you have no credit history or poor credit. Just open a loan account to “pay off” the loan into a certificate of deposit (CD) account.

The Self Visa reports to the major credit bureaus every month. This regular reporting to Equifax, Experian, and TransUnion allows users to quickly raise their credit score through a series of on-time payments. Because the card is linked to a Self Credit Builder Account, cardholders can increase their secured card credit limit as they continue to build their FICO Score with on-time payments. As your Credit Builder Account grows, that money can be moved toward your credit line with additional deposits.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Fair / Poor / Good

MastercardProcessing Network

$175 the first year; $49 thereafter. Monthly fee: $0 the first year (billed $0 each month); $150 annually thereafter (billed $12.50 each month)Annual Fee

Destiny Mastercard®

See termsRegular Purchase APR

See termsCash Advance APR

At a

Glance

The Destiny Mastercard is an ideal credit card for those with bad or fair credit who want the purchasing power of Mastercard but without the security deposit requirement of a secured credit card. With a modest annual fee and manageable initial credit limit, the Destiny Card doesn’t care about your credit past – instead, it helps you focus on your everyday expenses.

Best Benefits

Rates & Fees

Why Should You Apply?

A guaranteed $700 credit limit to help get your financial goals on track, if approved.

Apply with Confidence! There is no impact to your credit score if you’re not approved. See terms.

No security deposit, and a path to better credit.

Zero Fraud Liability - Peace of mind that comes with having a Mastercard.

Get the credit you deserve, even with less-than-perfect history.

An unsecured card great for everyday purchases

Regular Purchase APR:

See terms

Cash Advance APR:

See terms

Cash Advance Transaction Fee:

See terms

Annual Fee:

$175 the first year; $49 thereafter. Monthly fee: $0 the first year (billed $0 each month); $150 annually thereafter (billed $12.50 each month)

Foreign Transaction Fee:

1% of each transaction in U.S. dollars

Late Payment Penalty Fee:

See terms

Return Payment Penalty Fee:

See terms

Over Limit Penalty Fee:

See terms

You have an imperfect credit history, which may include a past bankruptcy

You have less-than-perfect credit

You want a Mastercard but don’t want to pay a security deposit

You want a credit card with the versatility to make foreign purchases

You plan to pay your statement in full every month

The Destiny Mastercard is a versatile “second chance” credit card thanks to its modest APR and initial unsecured $700 credit limit. While the Destiny Mastercard is all about repairing your credit, the card is still a fully-fledged Mastercard credit card.

The card compares favorably to both the Indigo Mastercard and the Milestone Mastercard – two other quality credit repair credit cards serviced by Concora Credit, Inc. And since those cards are always two of the most popular unsecured credit cards for bad credit, the Destiny is in great company.

Repairing your credit takes patience, persistence, and the right tools. While Destiny can’t force you to spend responsibly, it provides you with the right tools for the job of boosting your credit score. If you use your card to make small purchases, keep your credit utilization low, and pay your bill in full and on time each month, the Destiny Mastercard will do the rest.

Other Cards to Consider

Another type of “second chance” credit product is a merchandise card. Also known as a “catalog card,” merchandise cards offer an unsecured line of credit that is usable at specialty online stores.

An example of a merchandise card is the Boost Platinum Card from Horizon Card Services. The Boost Card offers successful applicants a $750 merchandise line of credit for use at the Horizon Outlet. What makes the card such a popular choice for credit builders, however, is the lack of hard inquiries when applying. Horizon Card Services does no credit checks when you apply, nor do they conduct an employment check. However, Horizon requires an active U.S. credit card, debit card, or checking or savings account to take part.

How to Choose the Best "Second Chance" Credit Card for Rebuilding Your Credit Score

When choosing a “second chance” credit card, there are a few key factors to consider. Here are some tips to help you choose the best credit card for rebuilding your credit score:

Check Your Credit Score: Before you apply for a “second chance” credit card, it’s a good idea to check your credit score. You can check your credit score for free online from reputable credit bureaus like Equifax or Experian. This basic credit information will give you an idea of where you stand and what credit cards you may qualify for.

Here are some helpful tips for finding your next credit repair credit card:

① Compare interest rates and fees

“Second chance” credit cards often come with a higher APR and more fees than traditional credit cards. It’s important to compare these rates and fees among different credit cards to find the best option. Look for a credit card with a low APR and reasonable fees.

② Get a credit card for subprime credit

Part of boosting your credit score is increasing your use of credit. For those with bad credit, this may seem counter-intuitive. Fortunately, there are many unsecured credit cards for poor credit and secured cards that can help you repair your credit score.

③ Pre-qualify to boost your approval odds

“Second chance” credit cards may have lower credit limits than traditional credit cards, so consider how much credit you need. Additionally, some credit cards may have higher approval odds than others, so consider your chances of being approved before applying – check out our guide to pre-qualifying for a credit card before applying

④ Always read the fine print

Before applying for a “second chance” credit card, read the fine print. Look for any hidden fees or terms that could impact your credit score or financial situation. Make sure you understand the terms and conditions before accepting and activating your new credit card.

Summing It Up

A “second chance” credit card can be a helpful tool for rebuilding your credit score. Using your credit card responsibly and making on-time payments can improve your credit score. With the right credit card and responsible credit use, you can rebuild your credit score and achieve your financial goals.

If you have a business, then you know getting organized can really help run things smoothly. Most importantly, coordinating your company finances in an orderly manner is of great benefit to any entrepreneur or business venture. Consider these tips to stay organized with your business’ finances.

Stay Organized With Your Business Finances

Running a business has various moving parts and amongst the many entrepreneurial duties, your business finances should absolutely be a priority. Stay organized and be on top of your business investments with a few tips.

Research and Plan

Get a good start on your business finances with a few simple actions. Use your business plan as a compass to guide you in the right direction. Include a section dedicated to your business finances such as in-depth figures and your financial goals.

In your research be sure to seek business resources. There are a variety of business programs that offer grants and guidance for business owners. These resources can be an excellent way to gain additional funding for your business, therefore assisting you in your finances.

In addition to preparing a business plan and seeking resources, prepare yourself to contribute a considerable sum of finances to your business. According to Shopify, business owners with zero employees spent $18,000 in their first year.

Create a Budget for Your Business

Similar to how you might have a budget for your personal finances, you will want to do the same for your business. Creating a budget for your business is a way to keep your spending in check. A budget prevents your from overspending and will help you as a business owner stays in control of your finances.

Ask yourself these important questions when creating a budget for your business:

How much capital do you have now and coming in soon?

What are your business’s fixed and variable costs?

Do you have funds set aside for future expenses or emergencies?

It is also recommended to create a financial statement that summarizes revenue, costs, and expenses, aka profit and loss (P&L) or income statement. The document is typically issued quarterly and annually for every business. Most importantly, if you plan on accessing resources via a business loan, the lender will request your business P&L statement.

Use Accounting Software

Maintain your business budget with the right accounting software. Using tools, like accounting software, to assist your business processes can help you save time and money. These kinds of software can help manage finances across the different areas of your business, such as:

cash flow

payroll

invoices

paying vendors on schedule

preparing you for tax time

Start a Business Bank Account

In similarity to creating a separate budget for your personal life and business, the same applies when opening a bank account for your business. A separate bank account from your personal savings is a good way to organize your business finances. Firstly, a separate bank account for your business will aid you in staying aware of your business cash flow.

Secondly, having a separate bank account for your business protects your personal assets from any legal action like lawsuits against your company. Additionally, you can also open several accounts under the same bank to keep your cash organized for different purposes like costs, salary, and taxes.

Pick the Best Business Credit Card for You

Not only do you need a separate bank account for your business, but you will also need a separate business credit card. Personal credit cards can be rewarding for personal purchases. However, business credit cards tend to offer a unique set of benefits and features for company expenses. Business credit card features may include the following:

Free expense management tools

Free employee cards

Helps build business credit score – essential for accessing future financing, insurance, etc.

Earn up to 7X points with seamless software integrations and no fees

Manage employee spending easily while earing 1.5% back on all purchases and paying no hidden fees

Don't let no credit keep your business from earning 3% back on all purchases

Make Reviews a Routine

Set your financial reviews as a priority. Devoting time to regular reviews will aid in keeping your finances in control and within budget. Although running a business can get hectic, you don’t want to leave your business financial reviews on the back burner. Set yourself at least a monthly reminder to get it done. Preferably on a more frequent basis, such as bi-weekly.

Don’t Have Time for Finances? Hire.

If you find yourself to be pressed for time when it comes to your business finances, it may be time to hire. Seek a professional or delegate the task to a trustworthy qualified person. If the amount of work your business requests of you is too much pressure, you may also want to ask for additional help.

Dining credit cards are just that – cards that offers savings, rewards, and discounts when dining out at a restaurant or ordering takeout. Dining or restaurant credit cards can help you save money on your next takeaway, earn points towards a vacation, or even get you an exclusive reservation that all your friends keep missing out on. Here’s everything you need to know about dining credit cards – from how they work, how to use them, how to find the best one for your lifestyle, and everything in between:

Table of Contents

At a Glance

Dining credit cards typically provide versatile rewards across multiple everyday spending categories.

Avoid paying an annual fee unless the rewards and bonuses surpass your average spending habits.

Subprime dining card options include bad credit, secured, and debit card products.