Last updated on February 20th, 2024

When you apply for a new credit card, the card issuer takes a variety of factors into consideration before approval. These factors can range from things like credit score, payment history, and the number of delinquencies on your credit report, to income, credit age, and the number of hard inquiries that appear on your credit reports.

Even when might think you’re a shoo-in for approval thanks to high credit scores, zero delinquencies and a squeaky-clean payment history, you might not be approved for the plastic you’re after. Perhaps one of the least-known, unofficial, rules that some banks follow when deciding approval is the “5/24 rule.” What exactly does 5/24 mean? If you’re looking for more information about the Chase 5 24 rule, you’ve come to the right place!

What is a Hard Inquiry?

A hard inquiry refers to the credit check that a lender performs before deciding whether to approve your application. This inquiry shows up on the credit report from all three credit bureaus, and typically will stay on your credit reports for two years. A hard inquiry is nothing to worry about, as it’s a common practice with all credit card issuers and lenders, although you’ll want to keep an eye on the number of hard inquiries you get. Here’s why:

What Exactly is the 5/24 Rule?

Every bank has rules that credit card applicants should know and follow. These rules are meant to ensure that credit card issuers do not get taken advantage of, and that they end up with long-term, profitable customers who will make payments on-time.

Chase Bank, perhaps the most stringent bank in the industry when it comes to approving credit card applicants, has implemented what is commonly referred to as the 5/24 rule. Chase’s 5/24 rule is relatively unknown but if it’s not on your radar when applying for new credit card offers, it could affect your application.

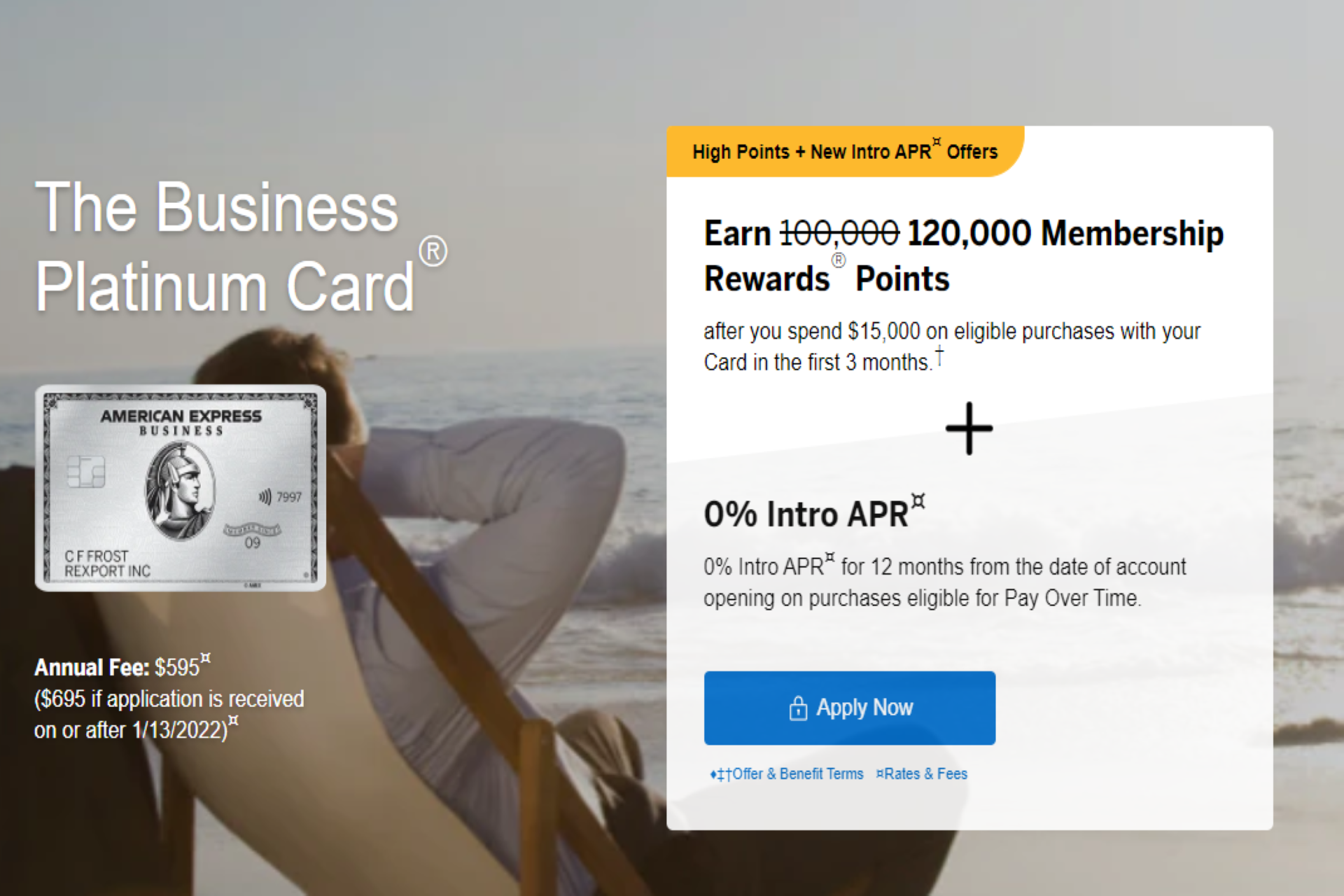

This is troublesome, considering Chase offers cards that feature extremely desirable cash back and travel rewards and even if your credit is in good standing and you are a strong candidate, you could be rejected for a new card based on this rule. These cards include a slew of excellent Chase personal credit cards that earn Chase Ultimate Rewards points – like the ultra-premium Chase Sapphire Reserve.

The 5/24 rule applies specifically to applicants who wish to open a new personal credit card with Chase. In a nutshell, the 5/24 rule stipulates that, if your account shows five or more credit card applications (which involve a hard inquiry each time you apply for a card) within the last 24 months, your credit card application will be rejected by Chase.

This rule applies to all personal credit cards and applications, from any bank or card issuer, that may appear on your credit report – not just to applications with Chase. This is an internal rule, one that Chase does not formally publish in their terms and agreements or via any official announcements; it came to light after people began to notice that they were denied for credit cards through Chase and took to online forums to discuss the reasons why, and to compare their experiences.

The rule was likely implemented as a means to combat credit card churning. While none of the above information is officially confirmed by Chase, beginning in November of 2018, more and more people began to report that they were being denied for nearly all Chase cards due to this rule; all info here is based on crowdsourced reports, and may be subject to change.

How Your 5/24 Status Could Affect You

For readers who haven’t opened a new credit card account in the last two years, most of this information is only pertinent once you begin to shop around for rewards cards and take advantage of the great offers that are out there. It helps to strategize before you begin applying for credit cards; select the top five card offers that appeal to you based on your wants and needs, choose your favorite, and apply for that card first.

There should always be some planning when dealing with finances, so spending the time to research your options beforehand won’t hurt! If you’ve applied to a Chase card and your application was rejected despite your good or excellent credit, this blog post may help to explain why. If you’ve applied for more than five credit cards within the past 24 months, you’ll have a difficult time applying for a personal credit card from Chase. At this point, you may throw in the towel and think that those lucrative card rewards are out of reach, but fear not!

What if I’ve Applied for More Than 5 Cards in 24 Months?

Some folks apply to multiple credit cards at a time because they think that due to bad credit, they won’t qualify for approval; it’s also possible that you were rejected for several offers, and sent an application for multiple cards in a short time frame because of this. Alternatively, many people apply to more than one card simply because they wish to take advantage of the various rich rewards plans available to the savvy consumer.

Either way, what do you do when you have at least five hard inquiries on your credit report in the past 24 months? If you’re above the 5/24 rule, don’t fret. While you’ll be limited in the card offerings available to you from Chase, other banks are not necessarily limited by this rule. Most card issuers have their own restrictions, and some may also implement the 5/24 rule – but it’s not universally applied across the industry, which means that you’ll have plenty of card options at your disposal. Take a look at what’s available from American Express or browse cards from banks like Wells Fargo and Bank of America, for example.

What if I’m an Authorized User on Someone Else’s Card?

If you’re an authorized user on someone else’s account (i.e. your spouse’s card), it will look like an open account on your own credit report. If you’re applying for a Chase card while you’re an authorized user on another account, this will count against you when it comes to the 5/24 rule, so it’s best to avoid becoming an authorized user if you’re applying to Chase credit cards at the same time.

What About Card Upgrades, or Conversions?

Some banks won’t report a card conversion or upgrade (also known as a product change) as a new account, especially if it’s within the same lineup as the existing account. It’s important to ask the card issuer if the application process involves a hard credit inquiry before completing an upgrade or conversion, since different banks will handle this in different ways.

If the bank confirms that a hard inquiry is part of the process to upgrade or convert your card, you’ll need to take into consideration whether you plan to apply for any Chase credit cards before you complete that change to your existing account.

Are There Any Exceptions to Chase’s 5/24 Rule?

It’s important to note that, while most cards will show up as a hard inquiry on your credit report when you apply for them, there are also cards that won’t count toward your total opened accounts. Exceptions to the rule include just about any Chase business card – most issuers will not report business card applications to the credit bureaus.

However, Capital One and TD Bank are two issuers that DO report business cards, so keep this in mind if you choose to apply for a business card and you’re close to five or more card applications that will show up on your credit report.

Who Can Apply for a Business Card?

In this day and age, it’s fairly easy to qualify for a business credit card, even if you don’t run a business! Next time you do some spring cleaning around the house, instead of throwing out the brick-a-brack, consider selling it on Craigslist or eBay.

Completing this sort of transaction can qualify you for a business card, believe it or not. Anyone who has a “side hustle” can apply for a business card, so if you sell your crafts on Etsy or drive for Uber to earn extra cash, you’ll be in the clear to open a business account.

How Do I Know My 5/24 Rule Status?

Many of us don’t think about the number of times we’ve applied for credit cards. Luckily, there are free tools available that give us insight into how many hard inquiries are on our personal credit reports.

Opening an account with Credit Karma, which is a free credit report service, can give us insight into the information necessary to figure this out. Some credit bureaus, like Experian, also offer free accounts that let you view your credit score. If you do plan to apply for multiple credit cards within a short time frame, it’s a good idea to keep track of each application date.

If you haven’t kept count, you can always check to see what the dates were by requesting to see any of your annual credit reports from your bank (or from the credit bureaus directly).