How Long Does It Take to Rebuild Your Credit Score?

When you’re ready to begin the steps to rebuild your credit score, it won’t take long to realize that there is no quick fix. Just as you need time to build up your initial score, you also need time to turn it around. So exactly how long does it take to improve a bad credit score to a good credit score? Unfortunately, the answer can vary.

Depending on the current state of your credit report and your financial strategy going forward, rebuilding credit can require anywhere from a few months to a year or more. Find out what can prolong credit improvement and ways you can nudge the process along below.

How Bad Credit Can Hurt You Financially

First, a refresher on the negative impacts of bad credit. Bad credit can negatively impact almost all aspects of your financial well-being. Having a trouble credit history can result in less access to unsecured, revolving credit, difficulty acquiring auto loans, mortgages, and other personal loans, higher interest rates, and potentially other hardships such as loss of employment opportunities (some employers check credit during the hiring process), or difficulty renting a new apartment.

Factors That Prolong Rebuilding Your Credit Score

Lenders typically send reports to credit bureaus on a monthly basis, though it can vary. This means it can take at least one month to see your score budge at all, let alone make a full recovery. Yet even if you start changing your financial habits today, previous actions can still significantly dampen your improvement efforts. Even worse, relying on misinformed ways to improve your credit score can hold you back further.

Negative Marks

The types of negative information you have on your credit report play a large role in how long it takes to rebuild your credit score. According to Experian, negative marks significantly affect your credit score and can linger on your credit report for years depending on your circumstances. For instance, a bankruptcy will remain on your report and affect your score for up to 10 years.

Account delinquencies, or missed payments, on the other hand, generally fall off after 7 years. If you’re dealing with either of these, it may take longer to boost your score than it would for someone with too many hard inquiries (when checking your credit score, which only stay on a report for 2 years).

Misinformation

Some people believe you need to carry a small balance from month to month to improve your credit. Unfortunately, misinformation like this can actually set you back and become costly in the long run. In the end, time and responsible credit card use are the best tools in your credit-building arsenal.

How to Improve Your Credit Score Fast

While there is no quick hack or trick for rebuilding your credit score, there are still plenty of ways you can take action. Time will allow your negative marks to lose their potency and eventually drop off. Meanwhile, strategic credit card use can help you create positive trends in your report and gradually boost your score.

Aside from paying off any outstanding debts, utilizing a credit card can often be the best way to improve a credit score. Of course, it can be difficult to even get one with a low score. For that reason, many companies offer credit cards specifically designed for credit improvement – and they aren’t all secured credit cards that require a deposit.

The Indigo® Platinum Mastercard® or Merrick Bank Double Your Line™ Platinum Visa®, for example, offer a quick and easy pre-qualification feature. This allows you to find out your likelihood for approval before you apply for a hard inquiry. Once approved, you automatically gain an unsecured $300 credit limit, though your creditworthiness determines your annual fee.

The credit limits with these cards may sound low, and that’s because they are – but that doesn’t mean cards like this can’t help you raise your credit. If you follow these simple guidelines, any credit-building card can work its magic on your score:

- Keep your credit utilization ratio down where you can. Even if you pay it off every time, maxing out your account often makes you seem high-risk.

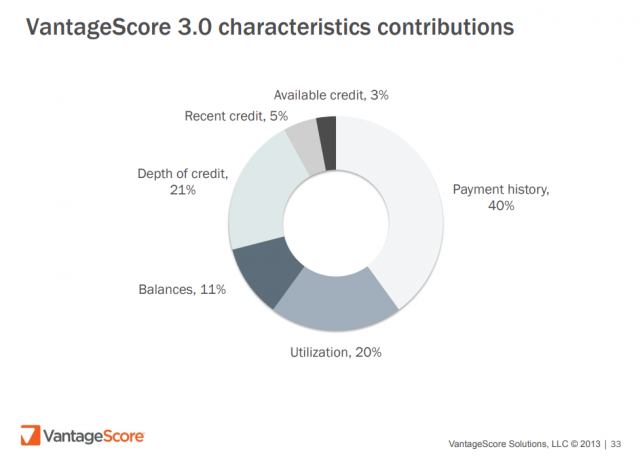

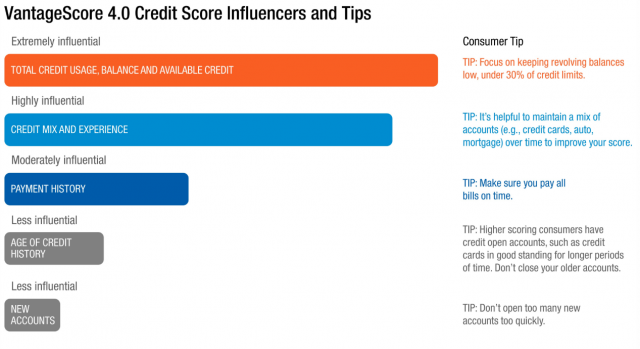

- Make your payments on time and consistently. always pay your bill on time. This is the most important, as payment history is the singe largest contributor to a FICO Score or VantageScore. This simple task improves your trustworthiness in the eyes of lenders and lowers your risk factor.

- Keep old credit accounts open, even if you aren’t using them. This makes it easier to manage your utilization ratio and can lengthen your credit history.

If you’re looking for a few more benefits and a potentially higher credit line in your card, Credit One Bank offers a number of impressive credit cards that provide Visa benefits like Zero Fraud Liability – plus rewards like cash back on certain purchases. Credit One also offers pre-approval to help you see if you qualify before applying.

Related Article: What Are the Easiest Credit Cards for Bad Credit to Get?