Credit Score Basics

A credit score is an essential aspect of your financial reputation. If you’re planning to buy a car, apply for a mortgage, or apply for a credit card, the financial institution you go to will consider your credit score before making a decision on your application. Read on to learn what a credit score is, what it’s made of, and how to interpret it. Here are some credit score basics:

Credit Score Basics: What is a Credit Score?

A credit score is a three-digit number that summarizes your credit history and represents how much of a risk you pose as a borrower of a lender’s funds. The higher the score’s number, the less likely you are to default on a loan or line of credit, and therefore, the more favorable your chances are of being approved for the loan or credit line. Better credit scores also mean lower interest rates and higher credit limits.

While a credit score does not paint the entire picture that is your credit history, it is a quick and reliable indicator of how financially responsible you are.

Credit Scores vs Credit Reports

Credit scores are determined based on your credit report, therefore they are not the same thing. Credit reports are created by the industry’s three major credit bureaus: Equifax, Experian, and TransUnion. Credit reports for an individual may vary slightly between these three agencies, so it’s not uncommon for each to assign distinct credit scores. When you apply for a credit card or loan, issuers will consider both your complete credit report along with your credit score as an overall assessment of said credit report.

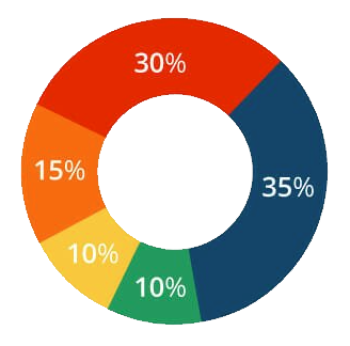

Credit Score Basics: What Makes Up a Credit Score

A credit score is comprised of a mixture of factors based on your personal information and previous, as well as current, financial activity. This data is available in your credit report. Payment history and current debt amount are the biggest determining elements when formulating one’s credit score, while credit history length, new credit, and credit mix make up the rest of the equation. Here’s a brief explanation of each:

|

Payment History |

Current Debt Burden |

Credit History |

New Credit |

Credit Mix |