Advertiser Disclosure – Credit cards and other offers on this site may be from companies from which BestCards.com receives compensation. This may determine which products are featured on the site, the pages where you may see them, and the order in which they may appear. However, such partnerships do not influence the opinions of our experts and we are not compensated for writing favorable reviews of our partners' products. Please note that, while we frequently publish new credit card reviews and other content, BestCards.com does not include every possible credit card available in the market.

According to Experian, one of the three major credit bureaus (along with Equifax and TransUnion), people with “exceptional” credit scores carry the most debt on average. Why is that, though? Here’s why people with good credit scores tend to have the most credit card debt.

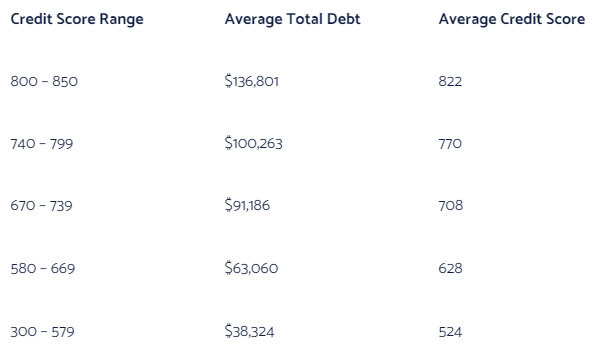

Excellent Credit and Debt: The Facts and Figures

Experian’s data shows a direct correlation between credit score and average debt. This data examines the average credit score and debt burden for consumers in Q2 of 2019.

Those with super-prime credit scores (a FICO score between 800 and 850) have an average total debt of $136,901, compared with an average total debt of just $38,324 for those with deep subprime credit (a FICO score between 300 and 579).

Many Consumers Mistakenly Believe High Debt Means Low Credit Scores

The report also notes that most American consumers have a mistaken belief that holding significant debt will directly harm your credit score. Over 80% of respondents held this belief, with 51% thinking higher credit scores had lower debt levels than those with bad credit scores.

Why Do Those with the Best Credit Have the Most Debt?

So, why are so many Americans confused about debt and credit scores? That’s because there is a general belief that debt is inherently bad. Sure, having it isn’t ideal, but managing it successfully and paying it off is an essential aspect of building an excellent credit score.

Payment History Is Essential to Excellent Credit

Payment history is the number one consideration when it comes to determining a FICO credit score. Because those with excellent credit scores have greater access to credit products (including credit cards), they have better odds of receiving new credit vs. those with fair or poor credit.

Having better access to credit creates the opportunity to amass more on-time payments, helping super-prime score holders to protect – and build – their credit score. People with deep subprime credit, on the other hand, have far fewer options, meaning they have less chance at accumulating debt.

More problematic, however, is the fact they all have more significant hurdles to boosting their credit score. Because of the importance of payment history, just one missed payment for someone with bad credit will have an exponentially greater impact than a similar event for a super-prime borrower.

How to Get a Better Credit Score

A string of on-time payments isn’t the only factor in getting excellent credit. There are several factors which must be met to improve credit and gain access to better credit opportunities in the future:

Reduce Credit Utilization

Credit use accounts for about 30% of a person’s FICO score, making it the second-largest factor in calculating that number (after payment history). A cardholder that doesn’t use more credit than they need to shows lenders that they can manage their monthly payments. A low credit utilization rate also displays that they aren’t stretched financially.

Keep Older Accounts Open

While the average age of credit accounts for only 15% of a person’s FICO score, keeping older accounts active is an easy way to build credit. Use credit cards at least once a year to keep the account active and consider downgrading if you have a card with an annual fee.

Editorial Disclosure – The opinions expressed on BestCards.com's reviews, articles, and all other content on or relating to the website are solely those of the content’s author(s). These opinions do not reflect those of any card issuer or financial institution, and editorial content on our site has not been reviewed or approved by these entities unless noted otherwise. Further, BestCards.com lists credit card offers that are frequently updated with information believed to be accurate to the best of our team's knowledge. However, please review the information provided directly by the credit card issuer or related financial institution for full details.