How to Repair Your Credit from Your Couch

Finding yourself in quarantine with nothing to do? Why not consider taking some steps to boost your credit score and improve your finances? Here are four helpful suggestions on how to repair your credit from your couch.

Monitor Your Credit Report

When repairing credit, the first thing a person should do is check their credit report and credit score. Your credit report details your complete credit history, allowing lenders to see how good of a borrower you have proven to be. If they don’t like what they see, your chances of boosting your credit could go up in smoke. Because of the importance of credit reports, you must make sure everything in yours is correct.

There are plenty of free credit score apps, plus quality paid services from leading names such as MyFICO, and TransUnion. While free services provide insight into your credit score, paid plans give you all the information on your credit report. These paid services also allow you to easily spot and dispute inaccuracies in your report, as well as comprehensive fraud monitoring and unlimited access to your credit reports 24/7.

Increase Your Credit Limits

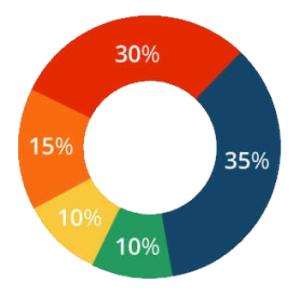

Part of understanding what your credit score is means knowing what factors impact your credit score the most. The FICO Score is the most popular scoring model, favored by over 90% of lenders.

FICO prioritizes five factors when determining a credit score:

- Payment history

- Credit utilization

- Credit history

- Types of credit

- New applications

Of these five factors, payment history and credit utilization are the most important, counting for 65% of your credit score. While payment history is relatively self-explanatory, credit utilization is slightly trickier.

Credit utilization refers to the total amount of your available credit you actually use versus your total credit limit. If you have a $1,000 credit limit, for instance, but use just $450 of it, that is a credit utilization rate of 45%. Ideally, you want to keep your credit use below 30% for maintaining credit – and below 10% for building credit.

Reduce Credit Utilization with a Secured Card

Repairing credit is all about getting the figures right. One of the easiest ways to decrease credit utilization is to increase your overall credit limit. One way to do this is to contact your current credit card companies and ask for a credit limit increase. For those with a good payment history and a long relationship, it might be as simple as a brief phone call. For those with imperfect credit, however, a secured credit card offers an excellent alternative.

Secured credit cards work by requiring a cash deposit. This deposit acts as the security for the lending risk and as the credit limit. The higher the deposit, the higher the credit limit. Because these cards require a deposit, they are much easier to get than other types of credit cards, making them great for quickly building credit.

Cards like the OpenSky Secured Visa require no credit check, meaning getting the card can’t hurt your credit score – only help it. Placing a large deposit on the card can quickly increase your available credit, and (with responsible budgeting and spending) reduce your credit utilization – quickly.

Consolidate Existing Debt

One of the biggest issues Americans face when repairing their credit is high-interest payments. Most credit cards feature an APR in the 15% to 25% range – or higher. Because of the burden credit card debt causes, paying off outstanding balances can seem impossible.

One of the easiest ways to reduce debt burdens is through consolidation. There are a variety of debt consolidation groups available, with rates considerably lower than what typically comes from a credit card. Groups like American Debt Enders are great for helping people find solutions for too much debt, for instance.

For those looking for a different approach, products like the Upgrade Card are another option. Upgrade works by extending a line of credit of up to $20,000 through their Visa credit card. The cardholder can then use that credit to pay off existing debts, consolidating them into one payment. Upgrade then converts the new balance into an installment payment plan of up to 60 months. Even better, interest rates with the card start as low as 6.99% – considerably lower than most credit cards on the market today.

Consider a Personal Loan

Like the Upgrade Card, personal loans typically offer lower interest rates than credit cards. These loans are another option for people looking to reduce their monthly payments and free up some of their budget for other things (including paying debt).

Many consolidations or personal loans are easy to apply for from your phone, laptop, or tablet, with decisions made in minutes. They also usually offer quick turnaround times, meaning the money can be in your bank account within the same day – or a few days at most. Some popular personal loan options include OppLoans, Smarter Loans, and Even Financial.