Last updated on February 20th, 2024

Is your New Year’s resolution to finally take the step towards becoming a homeowner? If so, you’ll likely need to build your credit score to qualify for a mortgage. Here is how to build credit to buy your first home.

Building Credit to Achieve Homeownership

Homeownership is one of the most common financial and personal goals of many Americans. However, buying a house, condo, or another property is an expensive proposition.

Home loans make this high cost achievable for millions of people every year. However, loans come with many of the same hurdles found in credit cards, auto loans, and other credit types. And, like different types of credit, building up your credit score to achieve the goal of homeownership takes time, patience, and knowledge.

What Credit Score Do You Need to Get a Home Loan?

First things first: What credit score do you need to reach before you can get a mortgage? According to Quicken, the minimum credit score required to qualify for a mortgage varies, but generally must be above a FICO Score of 500.

The credit score requirements for a home mortgage depend on the loan insurer, like FHA loans from the Federal Housing Administration, VA loans through the U.S. Department of Veterans Affairs, or conventional loans through lenders (like Quicken) or banks.

Here are the current minimum FICO credit score requirements for obtaining a home loan:

- Conventional loan – 620 minimum FICO Score

- FHA loan with 3.5% down payment – 580 minimum FICO Score

- FHA loan with 10% down payment – 500 minimum FICO Score

- VA loan – No federal minimum credit score requirement (many lenders require a FICO score of at least 620)

How to Build Your Credit Score to Buy Your First Home

Building credit to buy a home takes time. Ideally, this process should take between six months to one year, but it depends on your starting point – and determination.

Here are a few tips to help you quickly build your credit score:

Know Your Credit Score

Keeping up-to-date with your financial standing is essential for building a good credit score. Credit monitoring is even more critical for those looking to buy a home, as it instills confidence and reinforces the knowledge required to not only obtain a mortgage – but to handle it effectively, too.

There are many free credit monitoring services available, including those from banks and credit card lenders. There are also more thorough, paid services through FICO (MyFICO), Credit Karma, and more.

Related Article: Free Credit Score Monitoring from Card Issuers

Build Credit with a Credit Card

Once you know where your credit score stands, you can start to build that number through responsible credit use.

The easiest way to establish – and build – credit is through a credit card. Because there are plenty of credit cards for all credit scores (including secured cards or credit cards for bad credit), credit cards are the perfect way to raise your credit score quickly.

When choosing a credit card to build credit, here are a few things to look out for:

- When looking for a secured card, pay close attention to the annual fee, the APR, and the other fees associated with the card. Aim for an annual fee below $50, though the cards with the best interest rates typically fall within this cost range.

- Make sure your security deposit matches your expected credit card use. Do not place a $200 minimum deposit and max the card out, for example. Aim to use 30% of your available credit (or less) every month.

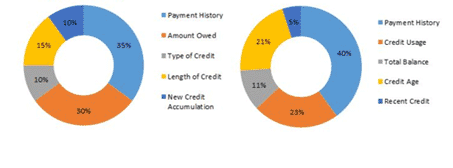

- Always pay on time. Payment history accounts for 35% of what makes up your FICO score. Even one missed payment can harm your score.

Build a Good Credit Mix

Lenders prefer to lend to borrowers with a robust combination of credit types. This fact is especially true when it comes to home loans and mortgages.

A “good credit mix” means a borrower has a demonstrable history with a variety of loan products. Since this is your first home, you may not have experience with home loans. Therefore, the best way to build a good credit mix is by having open – and current – loans like credit cards, student loans, personal loans, or auto loans.

A good mix of credit types shows a potential mortgage lender that you understand credit – and that they can trust you with an expensive installment loan.

Related Article: What Exactly Is a Good Credit Mix?

Other Things to Consider When Planning to Buy Your First Home

Buying a home does not just mean finding the right property and getting approved for the loan. There are other considerations to keep in mind when going through the home buying process. These considerations include:

- Saving for the down payment: All mortgages require a down payment. While FHA loans may allow down payments of as little as 3.5% on a home worth $100,000, that amount is $3,500. With the U.S. median home price currently at $320,000, saving $11,200 – or more – is a big hurdle to clear.

- Closing costs: Closing costs are another consideration to make. These fees are somewhat negotiable but can cost around 5% of the house’s sale price. These fees cover taxes, escrow, insurance, and other documentation and legal costs.

- Home repairs: The average homeowner may spend up to 5% of the home’s value on repairs within the first few years.

Related Article: Credit Tips: How Long Does It Take to Rebuild Your Credit Score?

Featured photo by Shopify / Burst