Aspiration Zero Card Seeks to Eliminate Carbon Footprint

Aspiration, a leading eco-conscious financial fintech and debit card issuer, has announced plans for its first credit card. The new product, set to launch later this year, will help cardholders reach carbon-neutral status with regular use. Here is what you need to know about the upcoming Aspiration Zero Card – the credit card designed to help users eliminate their carbon footprint.

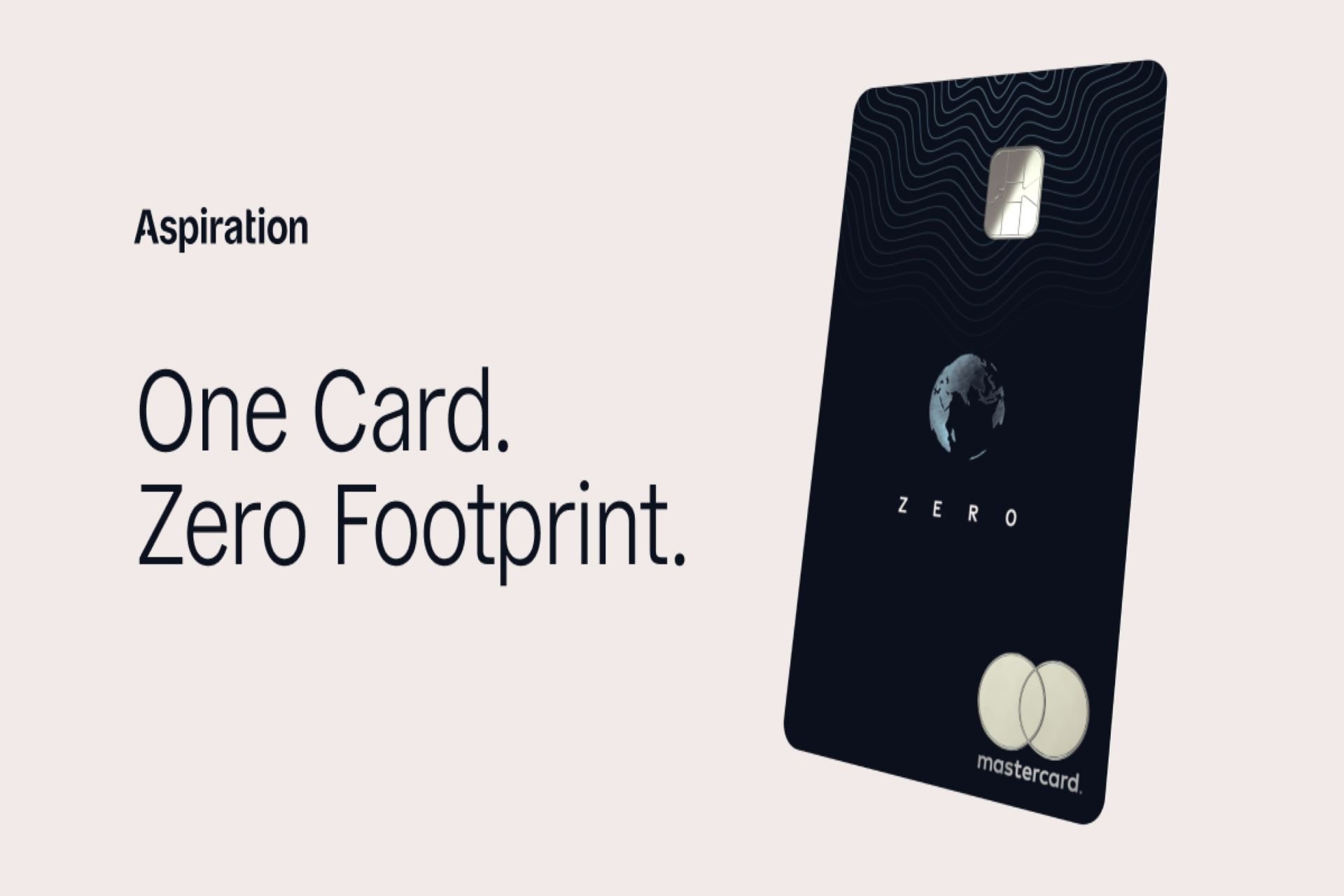

Aspiration Zero to Launch in 2021

Aspiration is launching its first credit card later this year. The product, called the Aspiration Zero, is a Mastercard that plants trees with every purchase. Aspiration has not set a date for the launch, but a waitlist is now available and is accessible at www.aspiration.com/zero.

For every signup to the waitlist from a personal referral, Aspiration will plant ten trees.

What Is the Aspiration Zero Card?

The Aspiration Zero is a credit card that makes a difference. The card works exactly like any other credit card, but it can help users reduce their carbon footprint with regular use.

Each time an account holder uses the Aspiration Zero Card to make a purchase, Aspiration will plant a tree through its global reforestation partners. Even better, by rounding up their purchase to the nearest dollar, cardholders can plant another tree – supercharging conservation efforts.

Like the card’s name implies, the Zero Card’s goal is to help account holders reach carbon neutrality. Doing this will come with additional benefits – including 1% cash back on all purchases for that month.

The Only Card That Rewards Taking Miles Off the Planet”

Speaking in a release announcing the upcoming launch, Aspiration co-founder and CEO Andrei Cherny highlighted the unique selling point of the Aspiration Zero – and the importance of conservation.

“There are plenty of credit cards out there that let you rack up miles; this is the only card that rewards you for taking miles off of the planet,” he said. “For the first time, you can have a climate change-fighting tool right in your wallet.”

About Aspiration

Aspiration is a leading platform helping people spend, save, shop, and invest, to both “Do Well” and “Do Good.” By bringing quality, ethical and sustainable financial products to all, Aspiration is on a mission to revolutionize the financial industry and change it for the better.

The company also issues a debit card that allows users to track their spending habits and see the card’s impact on the planet. The new Zero credit card is the latest entry into its “ecosystem of Clean Money products” that also includes accounts that help customers live free from fossil fuels.

In the past year, Aspiration customers have planted over five million trees. This planting rate and Aspiration’s commitment to plant 100 million trees in a decade make it one of the most prominent corporate sponsors of reforestation in the country.

Related Article: UBS Launches Credit Card Made of Corn