The long-anticipated Gemini Credit Card has finally arrived. Last month, the cryptocurrency platform, Gemini, reported the exciting news. The Gemini Credit Card is now available to eligible individuals in the US and offers crypto rewards for daily purchases. The card’s many features create a simple way for cardholders to integrate crypto investing into their everyday lives.

Gemini Crypto Rewards Card

The Gemini Credit Card was first announced last year with the option to join a waitlist. The list grew to more than 500,000 sign-ups, and it’s no surprise why. Those lucky enough to get approved will enjoy earning up to 3% back in crypto rewards. That is 3% back on dining (on up to $6,000 in annual spend and then 1%), 2% back on groceries, and 1% back on all other purchases.

Earning Rewards with the Gemini Credit Card

Similar to other cash back credit cards, the Gemini Credit Card earns up to 3% back on purchases dependent upon the purchase category. The difference: rewards are received in cryptocurrency. The earned crypto rewards from purchases made with the Gemini card are then automatically deposited into the cardholder’s Gemini account. The beauty is cardholders are not limited to one single type of cryptocurrency for their reward earnings.

Cardmembers choose from any of the 60+ cryptos supported by the Gemini platform, such as Bitcoin, Ethereum, Litecoin, and more. And you can switch reward types at any time, so you’re not tied down to one kind of crypto, thereby producing a more diversified portfolio. Furthermore, with the Gemini Credit Card, users will have access to the Gemini platform to buy, sell, trade, and store crypto.

Card Features

The Gemini Credit Card is made with 75% recycled stainless steel and comes in three colors – black, silver, and rose gold. The clean design of the cards is not just for looks; it also serves to keep cardholders’ information safe and private.

One of the many features of the Gemini Mastercard® is the option to transfer earned rewards into Gemini Earn, which is the company’s new interest-earning program. Gemini Earn program members can earn up to 8.05% APY on crypto held at Gemini, which is much higher than what traditional banks offer for fiat money.

Other Gemini Credit Card features:

No annual fee

Instant rewards

Security-first design

Instant access

World Mastercard® Benefits

24/7 live customer support

About Gemini

Gemini is a crypto exchange platform that has grown to build many secure cryptocurrency products. It was founded in 2014 by the investor twins, Cameron and Tyler Winklevoss. Gemini works to help individuals and institutions buy, sell, and store Bitcoin and other cryptocurrencies. It is a New York trust company regulated by the New York State Department of Financial Services. And it is also a fiduciary and Qualified Custodian.

Capital One has partnered with travel booking site Hopper to power the new Capital One Travel website. The partnership comes after a successful round of series F funding, led by Capital One. Here is everything you need to know about the new Capital One/ Hopper partnership and CapitalOneTravel.com.

Capital One Travel with Hopper

Capital One has a new travel portal exclusively available to Capital One Rewards credit cardholders. The bank has joining with travel portal Hopper to offer exclusive discounts to cardholders when booking travel online.

Hopper is a Canada-based travel website that raised more than $170 million in series F funding. That investment fundraiser was overseen by Capital One, which is now tapping Hopper for its new Capital One Travel website.

Capital One’s new partnership with Hopper will see the United States’ fourth-largest credit card issuer utilize Hopper’s unique interface to power CapitalOneTravel.com. Hopper differs from other travel booking platforms in that it uses artificial intelligence to tell consumers when they should book flights or hotels.

About Capital One Travel

CapitalOneTravel.com, powered by Hopper, launched in late 2021. The site provides a streamlined booking experience for Capital One Rewards cardholders, including the popular flagship Capital One Venture Card. Cardholders enjoy complimentary Price Drop Protection on flight bookings, meaning they’ll be refunded the difference for any additional changes to fares between booking and take-off. Customers will also enjoy the best price guarantee on flights, hotels, and car rental bookings.

Access to CapitalOneTravel.com is available to anyone with an eligible Capital One credit cardholder, namely those with a U.S.-issued Capital One Rewards card, including:

Eligible cardholders will also have access to Capital One Lounges at select airports across the United States. The card issuer is currently applying the finishing touches to three airport lounge locations: Dallas Fort Worth International Airport, Terminal D, Denver International Airport, Concourse A, Denver International Airport, Concourse A, and Dulles International Airport in the Main Terminal directly after TSA PreCheck.

Credit card debt is a crushing reality for anyone that doesn’t pay their credit card balance from month to month. Fortunately, knowing what interest charges are and how credit card interest is calculated can give you the knowledge to get out of debt faster. Here is everything you need to know about credit card interest – and how to avoid paying it.

How Credit Card Interest Works

Credit card interest is more than a monthly line item in your statement or a number printed on the credit card issuer envelopes you still receive via snail mail. Quite simply, it is the fee that you pay for the ability to borrow money. This interest rate is known as an annual percentage rate or APR.

Credit card issuers make a significant portion of their profits through interest payments. Suppose you carry a balance on your credit card. In that case, you can anticipate paying extra in addition to your overall purchase prices.

Credit card issuers calculate the interest you owe by multiplying the daily interest rate and adding it to your balance. This daily interest rate is your annual APR divided by the number of days in the year (365 in most cases).

Here is a quick example to demonstrate how to calculate your daily interest rate:

Credit card APR: 15%

Current balance: $500

Let’s say your current balance on your credit card is $500, and that card features a 15% APR on purchases. If you divide that 15% by 365, you’ll get a daily interest rate of 0.041%. This means that an outstanding balance of $500 would accrue $0.20 in interest every day. Should the balance remain the same for the whole billing period, you would owe $6.15 in interest at the end of the month, for a grand total of $506.15 owed.

How to Avoid Paying Interest

The easiest way to avoid paying interest is by paying your statement balance in full each month. Paying the full statement balance means avoiding interest, reducing your overall credit utilization, and ensuring your payments are never late or missed. When Should You Pay Your Credit Card Statement?

It would help if you always tried to pay your credit card by the due date every month. Most cardholders do this, but you can help your credit by paying your bill earlier in some instances.

Understanding when to pay your credit card bill requires a brief explanation of the credit card billing cycle. The credit card billing cycle encompasses the statement date, the due date, and the reporting date.

Statement Date: The statement date is the day your card issuer compiles all your transactions for the billing period and provides them to you in a statement. All purchases before this date are on your credit card bill, with all others occurring after that date posted to the next statement date.

Due Date: The due date on your credit card is the day you must pay at least your minimum amount due. The due date is typically three weeks after the statement balance posts.

Reporting Date: The reporting date is the final date in the statement cycle and refers to the day your bank reports to the major credit bureaus.This date may not be after your statement closes – in fact, it might be any time, so always ask your bank when they report to the major bureaus.

What is a Good APR for a Credit Card?

Interest rates on credit cards can vary significantly, depending on several factors:

Credit score and history

Is the credit card from a bank or a credit union?

Personal banking history with the card issuer

Does the credit card offer rewards?

Typically, the better your credit score, the lower your APR. Here are the current average APRs based on credit score:

Score

APR

Excellent Credit

24.49%

Good Credit

27.49%

Average Credit

29.24%

Bad Credit

31.74%

No Credit

29%

Because credit card APR can vary so widely, shopping around for the best credit cards is always advisable before applying. The easiest way to understand what interest rate you can expect is by searching for credit cards within your credit score profile. Keep in mind that the free annual credit report you receive at AnnualCreditReport.com does not provide a score, just your credit file.

How to Reduce Existing Credit Card Debt

Suppose you are concerned about your credit card balances and accruing too much interest. In that case, one solution is to consider a balance transfer credit card. Many of the best balance transfer cards feature promotional 0% intro APR periods of between six to 18 months. Introductory APR periods can halt further interest charges and help you pay down your current balances faster.

Here are the current longest 0% introductory APR periods on credit cards from the leading banks:

Interest is just the fee for the ability to borrow money, like the rent you pay to live in an apartment someone else owns or the charge for getting a ride downtown in someone else’s vehicle. It’s money you pay for convenience’s sake, though the overlying problem still exists.

Suppose you only make a minimum payment each month over the years. In that case, you may very well end up paying more in interest than the initial amount owed.

Irresponsible behavior (like not making your monthly payments on time) can also affect your credit scores, affecting things like the APR of cards you apply for in the future and even which ones you may qualify. If you can pay your credit card balance on time, every time, do it. You’ll be saving cash that can be used for more exciting aspects of life than interest.

Cash back credit cards are the most popular kind of rewards card and it’s easy to see why. Cash is versatile, practical, and straightforward to use, requiring far less fuss than what other types of rewards cards might warrant. Ranging from flat-rate rewards to bonuses for specific shopping categories, there are a lot of cash back cards to choose from— and this is where BestCards.com comes in. We have separated the best cash back credit cards from the rest of the pack to give you our top recommendations:

This post may contain links from partner offers, and we may receive compensation when you click on links to these offers. Please see our advertiser and editorial disclosures above for more information. Citi is an advertising partner.

Nowadays, credit cards come with all sorts of bells and whistles to convince you that they are worth applying for. There are cards that earn free hotel stays, free airfare, rewards with your favorite store, and even cards for discounts on gas. No matter how you tend to spend your money, cash offers the kind of reward that every kind of shopper can make use of.

Cash back is one of the best credit card rewards thanks to its versatility. Often, cardholders with a cash back card can opt for several redemption options for their rewards, including statement credits, gift cards, merchandise, travel, or even as a deposit into an eligible deposit account.

Thus, the versatility of cash back is tough to beat. Travel cards earn points or miles in loyalty programs, with these programs only providing select redemption options. Morever, points can only transfer to select partners – and if your points expire, they are gone forever. With cash back, rewards seldom expire.

What are the Best Cash Back Credit Cards?

Take a look at our top credit card selections for earning cash back this year:

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

$0Annual Fee

Citi® Double Cash Card – 18 month BT offer

18.99% – 28.99% (Variable)Regular Purchase APR

18.99% – 28.99% (Variable)Balance Transfer APR

29.99% (Variable)Cash Advance APR

At a

Glance

The Citi® Double Cash Card is one of the most versatile cash back credit cards on the market today, thanks to impressive, flat-rate cash back, lucrative introductory 0% APR offers, and more. Cardholders earn 2% back on every eligible purchase: 1% back at the time of sale and an additional 1% back when they pay their statement balance. Cash back is redeemable for statement credits, direct deposits, checks, or converted as ThankYou® points.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn 2% on every purchase with unlimited 1% cash back when you buy, plus an additional 1% as you pay for those purchases.

To earn cash back, pay at least the minimum due on time.

Balance Transfer Only Offer: 0% intro APR on Balance Transfers for 18 months. After that, the variable APR will be 18.99% – 28.99%, based on your creditworthiness.

Balance Transfers do not earn cash back. Intro APR does not apply to purchases.

If you transfer a balance, interest will be charged on your purchases unless you pay your entire balance (including balance transfers) by the due date each month.

There is an intro balance transfer fee of 3% of each transfer (minimum $5) completed within the first 4 months of account opening. After that, your fee will be 5% of each transfer (minimum $5).

Regular Purchase APR:

18.99% – 28.99% (Variable)

Intro Balance Transfer APR:

0% for 18 months on Balance Transfers

Balance Transfer APR:

18.99% – 28.99% (Variable)

Balance Transfer Transaction Fee:

3% of each transfer (minimum $5) completed within the first 4 months of account opening. A balance transfer fee of 5% of each transfer ($5 minimum) applies if completed after 4 months of account opening.

Cash Advance APR:

29.99% (Variable)

Cash Advance Transaction Fee:

5% of each cash advance; $10 minimum

Penalty APR:

Up to 29.99% (Variable)

Annual Fee:

$0

Foreign Transaction Fee:

3%

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $41

You prefer earning cash back at a flat rate rather than in rotating categories

You’re looking to either consolidate existing balances or pay down a large purchase with no interest charges for an extended period of time

You like to have the flexibility of converting cash back into lucrative rewards points

You’re considering a credit card without an annual fee

The Citi® Double Cash Card does not offer special rewards categories like the Citi Custom Cash Card. Instead, this product provides an unlimited 2% cash back on all eligible purchases. The card earns a flat-rate 1% cash back on all eligible purchases – and another 1% back when the account holder pays off that balance.

The lack of an annual fee, the prospect of 2% back, and the 0% introductory APR on balance transfers for the first 18 months make the Citi Double Cash Card the perfect everyday credit card for anyone who prefers not having to adjust their spending habits to get the most value.

Like the Custom Cash, the Double Cash from Citi earns rewards as ThankYou Points. Cardmembers can opt for statement credits, gift cards, merchandise, or other award options or use their points to book travel through Citi ThankYou® Rewards.

Another award option is to transfer ThankYou points to any of Citi’s 19 airline and hotel partners. Here is a quick breakdown of all of Citi’s transfer partners:

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

$0Annual Fee

Citi Custom Cash℠ Card

18.99% – 28.99% (Variable)Regular Purchase APR

18.99% – 28.99% (Variable)Balance Transfer APR

29.99% (Variable)Cash Advance APR

0% for 15 months on PurchasesIntro Purchase APR

At a

Glance

The Citi Custom Cash? Card is a generous cash back credit card that offers up to 5% back on eligible purchases. The card, from Citi, does not charge an annual fee and rewards 5% back on the top spending category each month, with options including transit, travel, gas, groceries, dining, and more.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

0% Intro APR on balance transfers and purchases for 15 months. After that, the variable APR will be 18.99% – 28.99%, based on your creditworthiness.

Earn 5% cash back on purchases in your top eligible spend category each billing cycle, up to the first $500 spent, 1% cash back thereafter. Also, earn unlimited 1% cash back on all other purchases.

No rotating bonus categories to sign up for – as your spending changes each billing cycle, your earn adjusts automatically when you spend in any of the eligible categories.

No Annual Fee

Citi will only issue one Citi Custom Cash℠ Card account per person.

Intro Purchase APR:

0% for 15 months on Purchases

Regular Purchase APR:

18.99% – 28.99% (Variable)

Intro Balance Transfer APR:

0% for 15 months on Balance Transfers

Balance Transfer APR:

18.99% – 28.99% (Variable)

Balance Transfer Transaction Fee:

5% of each balance transfer; $5 minimum.

Cash Advance APR:

29.99% (Variable)

Cash Advance Transaction Fee:

5% of each cash advance; $10 minimum

Penalty APR:

Up to 29.99% (Variable)

Annual Fee:

$0

Foreign Transaction Fee:

3%

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $41

You want to earn 5% back but do’t want quarterly categories

You plan on spending $1,500 within the first 90 days

You have a large purchase in mind that you want to pay down over time

You plan on transferring an existing balance within the first four months

The Citi Custom Cash℠ Card is an exceptional cash back credit card thanks to the fact that it earns up to 5% back. This is broken down as earning 5% on eligible purchases in the top spending category each month; options include transit, travel, gas, groceries, dining, and more. Here is the full slate of 5% back categories with the Custom Cash:

Important to note is that the 5% back categories are limited to the first $500 spent on eligible purchases in your top eligible spend category each billing cycle, with 1% back on all purchases thereafter. That spending cap is on par with other 5% cash back credit cards, namely the Discover It card, which cuts 5% rewards after the first $1,500 in spending per quarter.

Other noteworthy features of the Custom Cash credit card from Citi include:

Earn a $200 bonus in cash back after spending $750 on purchases in the first three months of account opening. This bonus also has a value of 20,000 ThankYou Points, the official currency of Citi proprietary rewards cards.

0% intro APR for 15 months on purchases and balance transfers

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent

VisaProcessing Network

NoneAnnual Fee

U.S. Bank Cash+® Visa Signature® Card

19.74% to 29.74% variable based on creditworthiness and the Prime RateRegular Purchase APR

19.74% to 29.74% variable based on creditworthiness and the Prime RateBalance Transfer APR

29.99% variable based on the Prime RateCash Advance APR

0% for 15 months from account openingIntro Purchase APR

At a

Glance

The U.S. Bank Cash + Visa Signature Card is an excellent cash back credit card that gives holders the power to decide how they earn their cash back. The card earns 5% back on two select categories you choose, 2% back on one “everyday” category a user selects, and 1% back on all other purchases.

Best Benefits

Rates & Fees

Why Should You Apply?

New! $200 bonus after spending $1,000 in eligible purchases within the first 120 days of account opening

5% cash back on your first $2,000 in combined eligible purchases each quarter on two categories you choose

5% cash back on prepaid air, hotel and car reservations booked directly in the Rewards Travel Center

2% cash back on one everyday category, like Gas Stations/EV Charging Stations, Grocery Stores or Restaurants

1% cash back on all other eligible purchases

No Annual Fee

Pay over time by splitting eligible purchases of $100+ into equal monthly payments with U.S. Bank ExtendPay™ Plan

Terms and conditions apply

Intro Purchase APR:

0% for 15 months from account opening

Regular Purchase APR:

19.74% to 29.74% variable based on creditworthiness and the Prime Rate

Intro Balance Transfer APR:

0% for 15 months on transfers made within 60 days from account opening date

Balance Transfer APR:

19.74% to 29.74% variable based on creditworthiness and the Prime Rate

Balance Transfer Transaction Fee:

Either $5 or 3% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.99% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Foreign Transaction Fee:

2% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $41

You want the ability to choose your enhanced cash back categories

You like the freedom of switching categories each quarter

The U.S. Bank Cash+™ Visa Signature® Card is an excellent cash back credit card for those who want the power to decide where they earn their rewards. The card is similar to the Citi Custom Cash in that it offers cardholders up to 5% back on the first $2,000 in combined eligible purchases in the following categories:

TV, internet, and streaming services

Cell phone providers

Electronics stores

Fast food

Home utilities

Furniture stores

Department stores

Clothing stores

Movie theaters

Ground transportation

Fitness centers

Sporting goods stores

As mentioned, that 5% back is limited to the first $2,000 in spending each quarter, which is very generous. Cardholders also have the same option with their 2% “everyday” category, selecting one of the following three categories each quarter:

Grocery stores

Gas stations

Restaurants

The ability to customize your cash back options – and change them each quarter – is an excellent feature that helps to maximize the cash back potential of this card.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent

MastercardProcessing Network

$95Annual Fee

Capital One® Savor® Cash Rewards Credit Card

19.99% – 28.99% variable based on creditworthiness and the Prime RateRegular Purchase APR

19.99% – 28.99% variable based on creditworthiness and the Prime RateBalance Transfer APR

29.99% variable based on the Prime RateCash Advance APR

At a

Glance

Make memories while funding future adventures with the Capital One® Savor® Cash Rewards Credit Card. This exclusive entertainment credit card boasts an unlimited 4% cash back on streaming, dining, and entertainment is a great card for couples, families, and social butterflies.

Best Benefits

Rates & Fees

Why Should You Apply?

Unlimited 4% cash back on dining, entertainment, and popular streaming services

Earn 3% at grocery stores

Earn 1% on all other purchases

Earn 8% cash back on tickets through Vivid Seats

Receive $9.99 statement credit after paying for Postmates Unlimited membership

Enjoy comprehensive, personalized assistance in dining, entertainment and travel— 24 hours a day, 365 days a year

Regular Purchase APR:

19.99% – 28.99% variable based on creditworthiness and the Prime Rate

Balance Transfer APR:

19.99% – 28.99% variable based on creditworthiness and the Prime Rate

Balance Transfer Transaction Fee:

3% of the amount of each transferred balance that posts to your account at a promotional APR that we may offer you. None for balances transferred at the Transfer APR

Cash Advance APR:

29.99% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 3% of the amount of each cash advance, whichever is greater

Annual Fee:

$95

Late Payment Penalty Fee:

Up to $40

You want to earn an unlimited 4% cash back on streaming, dining, and entertainment, 3% at grocery stores, and 1% on all other purchases

You see yourself spending $3,000 within the first 3 months of opening the card to earn that one-time $300 cash bonus

You live for unique dining, entertainment, and sports experiences

You want complimentary food delivery membership through Postmates

Capital One has done a superb job of creating a credit card for entertainment; in other words, fun things. This is a rewards category left largely neglected by the industry. With the Savor® Rewards Card, cardholders will earn an unlimited 4% cash back on dining and entertainment, as well as a less exciting – but still practical – 2% at grocery stores.

The broadly defined “entertainment” category includes most memory-making outings, such as sporting events, movie theaters, and live concerts. This expansive category makes this card equally useful for families or young cardholders who frequently look for activities to take part in with their friends.

The Savor Card does carry a $95 annual fee, but the person who spends about $200 a month on outings or dining (or a total spend of $2,475 a year) will quickly recoup the card’s cost. Aside from the card’s generous bonus categories, Capital One’s cash back redemption portal is second-to-none and one of the most user-friendly rewards programs in the industry.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

American ExpressProcessing Network

$0 for the first year. Then $95Annual Fee

Blue Cash Preferred® Card from American Express

19.24% to 29.99% variable based on creditworthiness the Prime RateRegular Purchase APR

19.24% to 29.99% variable based on creditworthiness the Prime RateBalance Transfer APR

29.99% variable based on the Prime RateCash Advance APR

0% for 12 months from account opening dateIntro Purchase APR

At a

Glance

Through the Blue Cash Preferred® Card from American Express, you can earn sizable cash back rewards on purchases in common categories, including 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1%), 3% cash back at U.S. gas stations and select U.S. department stores, and 1% on all other purchases. You can also earn $300 back in the form of a statement credit after you make $3,000 in purchases using your new card in the first six months of the account being open.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn a $300 statement credit after you spend $3,000 in purchases on your new Card within the first 6 months.

$0 intro annual fee for the first year, then $95.

Buy Now, Pay Later: Enjoy $0 intro plan fees when you use Plan It® to split up large purchases into monthly installments. Pay $0 intro plan fees on plans created during the first 12 months from the date of account opening. Plans created after that will have a monthly plan fee up to 1.33% of each eligible purchase amount moved into a plan based on the plan duration, the APR that would otherwise apply to the purchase, and other factors.

Low Intro APR: 0% on purchases and balance transfers for 12 months from the date of account opening. After that, your APR will be a variable APR of 19.24% – 29.99%. Variable APRs will not exceed 29.99%.

6% Cash Back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%).

6% Cash Back on select U.S. streaming subscriptions.

3% Cash Back at U.S. gas stations and on transit (including taxis/rideshare, parking, tolls, trains, buses and more).

1% Cash Back on other purchases.

Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit

Get up to $120 in statement credits annually when you pay for an Equinox+ membership at equinoxplus.com with your Blue Cash Preferred® Card. That’s $10 in statement credits each month. Enrollment required.

Thinking about getting The Disney Bundle which includes Disney+, Hulu, and ESPN+? Your decision made easy with $7/month back in the form of a statement credit after you spend $12.99 or more each month on an eligible subscription with your Blue Cash Preferred Card. Enrollment required.

Terms Apply.

Intro Purchase APR:

0% for 12 months from account opening date

Regular Purchase APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Intro Balance Transfer APR:

0% for 12 months from account opening date

Balance Transfer APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Balance Transfer Transaction Fee:

Either $5 or 3% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.99% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Penalty APR:

29.99% variable based on the Prime Rate

Annual Fee:

$0 for the first year. Then $95

Foreign Transaction Fee:

2.7% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $40

Return Payment Penalty Fee:

Up to $40

You budget for family spending and want a credit card that earns significant cash back

You’ll spend a lot of money on groceries to take advantage 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1% after that)

You’re excited at the prospect of earning 6% cash back with select streaming services

You want to capitalize on your commute with 3% cash back at U.S. gas stations (and select U.S. department stores)

You’ll take advantage of 3% cash back on transit (taxis/rideshare, parking and tolls, trains, buses and more), and 1% on all other purchases

You’re likely to make $3,000 in purchases within the first six months of the account opening to qualify for a one-time $300 statement credit

You cook at home often and commute to work and school regularly, or make use of public transit regularly

There is no shortage of credit cards that offer rewards for everyday necessities like gas and groceries. Still, the Amex Blue Cash Preferred® Card remains one of the best cards for this task. Earning an unprecedented 6% cash back on U.S. supermarkets and select streaming services, plus 3% back on U.S. gas station purchases and 1% back on all other purchases.

Keep in mind that the 6% back on groceries is capped at $6,000 per year in purchases, with all groceries earning 1% back after that threshold is met. The Blue Cash Preferred carries a $95 annual fee that is easily justifiable for the person who spends at least $132 in groceries per month (or $1,584 a year). Cardholders will also earn a competitive 3% cash back on other everyday necessities such as gas, transit (including rideshares), parking, tolls, and public transit.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

NoneAnnual Fee

Chase Freedom Flex

19.74% to 28.49% variableRegular Purchase APR

19.74% to 28.49% variableBalance Transfer APR

29.49% variable based on the Prime RateCash Advance APR

0% for 15 months from account opening dateIntro Purchase APR

At a

Glance

The Chase Freedom Flex is a hybrid cash back credit card that offers something for everyone. The card earns 3% cash back on dining and drugstore purchases, plus up to 5% back on rotating categories each quarter after activation – all for no annual fee.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn a $200 bonus after you spend $500 on purchases in the first 3 months from account opening

Earn 5% on up to $1,500 on combined purchases in bonus categories each quarter you activate

Earn 5% on travel purchased through Chase Ultimate Rewards

Earn 3% on dining at restaurants, including takeout and eligible delivery services

Earn 3% on drugstore purchases

Earn 1% on all other purchases

0% Intro APR for 15 months from account opening on purchases and balance transfers, then a variable APR of 19.24%-27.99%

No annual fee – You wo’t have to pay an annual fee for all the great features that come with your Freedom Flex℠ card

Intro Purchase APR:

0% for 15 months from account opening date

Regular Purchase APR:

19.74% to 28.49% variable

Intro Balance Transfer APR:

0% for 15 months from account opening date

Balance Transfer APR:

19.74% to 28.49% variable

Balance Transfer Transaction Fee:

Intro fee of either $5 or 3% of the amount of each transfer, whichever is greater, on transfers made within 60 days of account opening. After that: Either $5 or 5% of the amount of each transfer, whichever is greater.

Cash Advance APR:

29.49% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Penalty APR:

Up to 29.99%

Foreign Transaction Fee:

3% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $40

Return Payment Penalty Fee:

Up to $40

You want a versatile cash back credit card that earns rewards across various categories

You don’t mind the lower cash back rates for dining and drugstore purchases over previous Chase cards

You prefer to book travel through Chase Ultimate Rewards

You don’t want to pay an annual fee for premium Mastercard features

The Chase Freedom Flex World Elite Mastercard earns 5% cash back on rotating categories each quarter after activation, 5% back on travel booked through Chase Ultimate Rewards, 3% back on dining and drugstore purchases, and 5% cash back on eligible gas station purchases on up to $6,000 spent in the first year. The card’s rotating categories are always popular, with 2023 already providing some versatility for card members.

Here is Chase’s Cash Back Calendar for 2023:

Date

5% Cash Back Category

Q1

January – March 2024

Grocery stores (excluding Walmart), self-care and spa services, plus fitness and gym memberships

Q2

April – June 2024

Restaurants, hotels, and Amazon.com and Whole Foods purchases

Q3

July – September 2024

Gas, EV charging, select live entertainment, and movie theatres

Q4

October – December 2024

PayPal, McDonald’s, pet shops and veterinary services, plus select charities

For those unsure if the Flex and its rotating categories are right for them, the Freedom Unlimited (or even the previously mentioned Citi Double Cash) might be a better bet.

FAQs About a Cash Back Rewards Credit Card

Here are answers from some of the most asked questions about cashback credit cards:

Cash back credit cards are like any other rewards card. You make a purchase, and you get rewards in the form of points. Unlike other rewards cards, however, these credit cards offer the best redemption options as cash awards. These awards take the form of deposits into bank accounts, statement credits, or gift cards.

Some card issuers, like Discover, offer a cashback match after the first year. A cash back match is when the bank automatically doubles your cash back after a set period. If you earn $100 in cash rewards, for example, the bank will double that to $200 – automatically.

Points and cash back are mostly the same. All rewards cards earn points. Some cards, however, offer better redemption value for different options. Cards like the Chase Sapphire Cards are much better at earning travel rewards than the Blue Cash Preferred Card from American Express, for example.

The time for points or cash back to show up in your account varies based on the transaction and the card issuer. Most transactions appear in your account within a few days after the purchase clears, but sometimes cash back might not show up for a week or so. If you still do not see your cash back rewards after several weeks, contact your card issuer to get clarification.

Some card issuers have limits on the minimum amount of rewards before cardholders can cash out. Others, however, have no minimum requirements. Deciding when to cash out is a personal decision. Many experts believe that redeeming cash back every month is an excellent habit to get into, as it can help reduce monthly payments and boost the amount of cash you have for everyday spending.

Looking to find the best credit cards for bad credit? The BestCards team has you covered with our guide to the top choices for rebuilding a damaged credit score.

Credit card sign-up bonuses and rewards points often get the most hype when attracting new applicants, but a 0% intro APR is one of the best promotions available on a credit card. What does 0% introductory APR mean, and what should you look for in a 0% intro APR balance transfer credit card? Here is everything you need to know about 0% intro APR credit cards:

This post may contain links from partner offers, and we may receive compensation when you click on links to these offers. Please see our advertiser and editorial disclosures above for more information. Citi is an advertising partner.

What is a 0% Intro Credit Card?

Zero-percent introductory APR credit cards (sometimes stylized as “0% intro APR” or “0 APR” allow cardholders to make purchases, balance transfers, or both for a set period without worrying about accruing any interest if they make the minimum payment each billing cycle. Having a card with a 0% can greatly benefit anyone hoping to make a big purchase or pay down existing debts, provided the terms and conditions are carefully followed.

What Is the Longest 0% Intro APR Period?

Here are the current longest 0% introductory APR periods on credit cards from leading issuers:

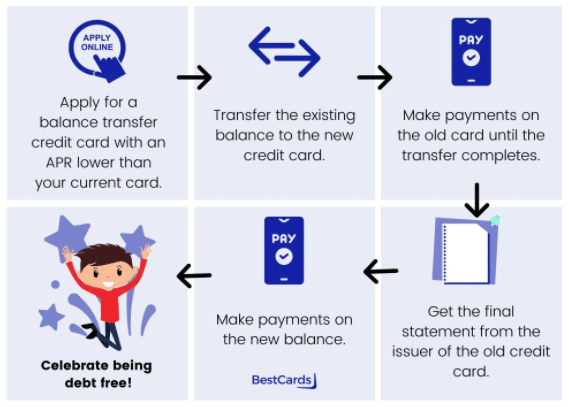

A balance transfer uses one credit card to pay off the debt accumulated on another credit card, often at a much lower monthly payment due to reduced interest costs. The best way to begin this process is to compare the introductory period balance transfer APRs of the credit cards you’re interested in. Once this is done, you apply for the new credit card and submit a request to transfer your balance to the new card issuer.

Here is a helpful breakdown of the balance transfer process:

What are the Benefits of Credit Cards with 0% Intro APR?

Credit cards with introductory APR periods provide significant benefits to cardholders. These benefits include:

Pay Down Debt Faster

Cardholders who have multiple credit cards with stacking up balances and spiraling interest rates can use a balance transfer card to consolidate all their debt onto a single card. They can pay off these balances without worrying about interest for an extended period.

If you do this, you’ll have to pay a fee each time you transfer a balance. Still, there’s a good chance these balance transfer fees will be less than the interest you’d accrued had you tried paying off each card individually.

Better Credit Scores Get Better Rates

Having excellent credit usually entitles you to better (lower) interest rates and larger credit limits. This rule applies to low APR, 0% intro APR, and balance transfer credit cards.

Statistics show that the better your credit score, the better you’ll enjoy a credit card with 0% intro APR – especially on balance transfers, as seen below:

Credit Score

Balances Transferred

% of Balances Transferred

Excellent

$38.8 million

72%

Good

$13.5 million

25%

Subprime

$1.62 million

3%

Someone with good or excellent credit transferred more than 95% of all balances, according to these Consumer Finance Protection Bureau (CFPB) statistics. The exceptionally low APR of many of these cards for people with Prime or Super-Prime credit simply cannot be ignored when it comes to benefits with these credit cards.

Pay for Emergency (or Expected) Expenses

Introductory APR periods aren’t just for balance transfers. Many credit cards offer a promotional APR on both purchases and balance transfers, including cards like the Discover it Cash Back, the aforementioned Citi Diamond Preferred and Simplicity, and the Wells Fargo Reflect Card. All of these offer 0% APR on both purchases and balance transfers. While the no-interest period may differ between the cards (in terms of length), having two interest-free periods is undoubtedly better than one.

Credit cards offering 0% interest on purchases can greatly benefit consumers – if they use them properly. They can easily pay off transactions over time, not having to worry about any interest for several months, which can help cardholders planning to make a big-ticket purchase. Plus, if an emergency were to occur, such as a needed auto repair or a medical emergency, an interest-free credit card can ease the burden of a big bill into multiple payments.

Rewards

The benefits of 0% introductory APR credit cards aren’t just limited to the lack of interest rate. It’s not uncommon to find a credit card offer that gives cardholders extra perks such as rewards – including cash back rewards – or travel insurance.

Potential Downsides to 0% Intro APR Credit Cards

While balance transfer and 0% intro APR credit cards offer significant value, some drawbacks might cause more costs than benefits to the primary account holder.

Balance Transfer Fees

Most balance transfer cards charge a balance transfer fee. Sure, you might enjoy 0% APR on balance transfers, but you’ll get charged a one-time fee for making that transfer.

The average balance transfer fee with a credit card tends to be $10 or 5% of the total amount transferred, whichever is greater. For example, if you plan to transfer a $5,000 credit card balance to a new 0% APR credit card, you can expect to pay $250 in fees.

Some banks provide special promotional balance transfer fees, such as Capital One. Others charge no fees if a transfer is made within a set period, usually within three months of opening an account. Always read the terms & conditions of your credit card before transferring a balance to understand better the fees associated.

Not Paying Off the Transferred Balance Before the Promotional Period Ends

The biggest drawback of a 0% introductory APR credit card is potentially carrying a balance past the introductory period and accruing interest. If you make a big purchase and take the balance past the 0% introductory APR period, your purchase will become more expensive as time passes due to the accruing interest.

The same principle applies to balance transfers. Once the promotional 0% introductory APR period expires, you’ll have to pay interest on the remaining balance – thus slowly eroding the progress had you paid off the card during the initial period.

Missing a Payment

Always read the terms & conditions carefully before applying. Missing a payment with an introductory APR credit card might lead to forfeiture of any promo APR. While this isn’t true with every credit card, some offers may include language that requires all payments to be made on time to ensure the 0% APR applies throughout the promotional period.

Penalty APR is a particular interest rate applied for missing your monthly payment and grace period. Typically a penalty interest rate lasts for at least six months to a year and is around 29.99%, but could be higher.

Insufficient Credit on the New Credit Card

Another potential drawback is underestimating how much credit you’ll be approved for. Credit limits vary by lender and by credit profile of the applicant.

How much credit you’ll receive can depend on several factors:

Relationship with the bank (including current credit limits)

Number of new accounts opened in the last year

Number of hard inquiries on your credit report within the last two years

Credit score

Credit utilization ratio

Before applying for a 0% intro APR credit card, make sure you can afford to repay the current balance through the existing credit card before applying for a balance transfer or low rate card. This process will ensure you are financially stable should your credit card application get rejected.

Other Downsides

The potential for unchecked spending is another downside of credit cards offering special interest rates. The cardholder could spend more and more on the card while the timeframe to pay off the balance interest-free dwindles month by month.

APR might not apply to both purchases and balance transfers

Your store card balance might not transfer in some instances

What Should I Look For in a 0% Introductory APR Credit Card?

Before applying, do you know what to look for in a 0% introductory APR credit card? Here are a few things to keep an eye on:

Length of Interest-Free Introductory Period: How long is the 0% APR period? Understanding exactly how long your interest-free period runs is vital to getting the right credit card for your needs.

What Does the Intro APR Cover? Does the introductory period apply to balance transfers or purchases – or does it apply to both? Before applying for a credit card, ensure you understand what is covered.

Ongoing APR: Rates usually vary depending on your credit score. The better your credit score, the better your regular APR after the promotional period will be.

Annual Fee: Does the card have an annual fee? No annual charge means one fewer cost for you, especially if you plan to keep the card for a long time.

Rewards: Many rewards credit cards come with an introductory APR bonus offer on purchases, but rarely on balance transfers. Keep an eye out for rewards cards that provide an intro APR on BTs, such as the Citi Double Cash Card.

The Star Alliance will become the first major airline alliance to issue its own co-branded credit card. The news comes as the alliance celebrates its 25th anniversary. Here is what we know so far about the Star Alliance credit card:

Star Alliance to Launch Credit Card Later This Year

The Star Alliance will launch a co-branded credit card later this year. The credit card news came as Star Alliance celebrates its 25th anniversary this month, following an agreement between United Airlines, Scandinavian Airlines, Thai Airways, Air Canada, and Lufthansa on May 14, 1997.

While an airline credit card is nothing new, an airline credit card co-branded with an airline alliance is. None of the “big three” alliances (Star Alliance, SkyTeam, and Oneworld) offer a streamlined credit card that allows cardholders to earn miles and points applicable across all brands. Star Alliance member Lufthansa does offer a co-branded card through Miles & More, its codeshare brand, but this is an outlier – and not the norm.

Very few details are known regarding the upcoming credit card. However, here is what we do know:

The card will launch in an unspecified “regional market.”

The card will be convertible into a Star Alliance member carrier frequent flyer program of the cardholder’s choice

“Exciting, Industry-First Offers”

“We reflect on the successes of Star Alliance in uniting the leading global airlines, with an eye firmly focused on a future where the customer continues to be at the heart of our work and our global network,” said Jeffrey Goh, CEO of Star Alliance, about the news.

“I am very excited for the innovations led by Star Alliance and our member carriers as we aim to be the most digitally advanced airline alliance offering seamless travel experiences with a unique loyalty proposition.

“This year, we look forward to further developments in seamless connectivity – such as new digital and mobile innovations – and exciting industry-first offers that loyal customers of our member carriers will welcome.

“We have defined the way the Earth connects for years, and now more than ever, is the time to enable technology to provide seamless journeys and delight the loyal customers of our member carriers.

“I am happy that ‘Together. Better. Connected.’ – our new tagline – reflects that earnestly and is also future-facing. It will motivate us to do better.”

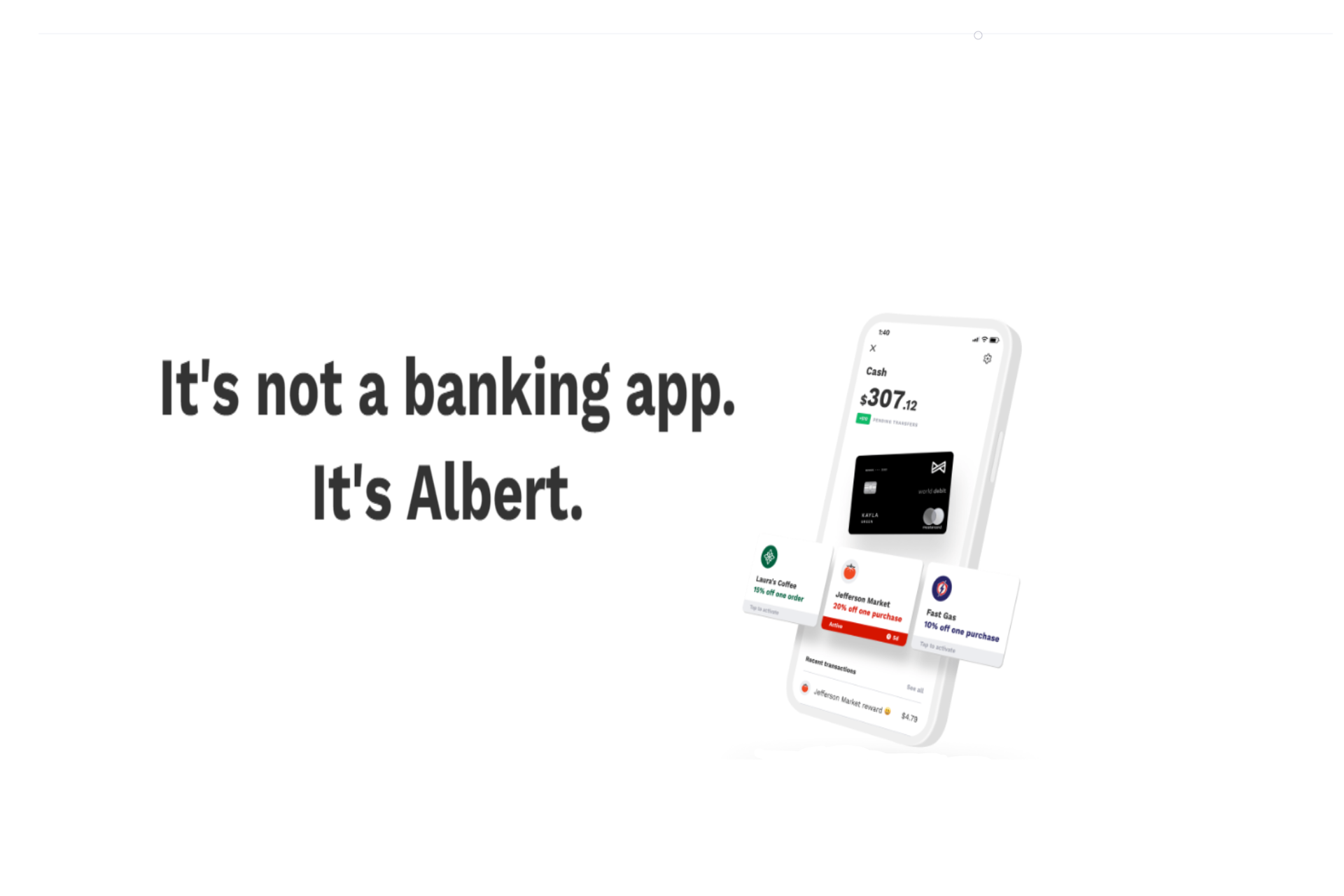

Thanks to its “We’re Banking on You” ethos and unique digital platform, Albert is the first company to bring high-touch personalized banking to everyone. Albert combines banking, savings, investing, and budgeting with Albert Genius, a team of finance experts who provide advice on any financial topic instantly by text. But what is Albert, and is it for you?

What is Albert?

Albert is a wealth management service and financial app that provides automatic savings tools and accounts, cash-back rewards, auto-investment, and other features. Albert operates on a “pay-what’s-fair” pricing model, with monthly fees starting as low as $0.

Opting for the premium tier, which costs between $4 and $14 per month, brings additional features, such as cash back rewards, investment accounts, and access to Albert Genius, Albert’s financial professionals. The Albert Genius team responds to tens of thousands of member queries per day, ranging from answering personal finance questions to providing one-of-a-kind support for Albert’s app.

Albert Features

The Albert app (available on Google Play and Apple App Store) provides an integrated platform for member needs. Here are Albert’s key features:

Albert Cash: Albert Cash is a bank account where everything comes together: spending money, budgeting, automatic saving, cash back rewards, and more. Features of Albert Cash include $0 minimum balances, $0 maintenance fees, up to 20% cash back, getting paid up to 2 days early, sending and depositing checks, 55,000 free ATMs, and more. The account also comes with the Albert Mastercard®, the associated Mastercard debit card.

Smart Savings: Albert analyzes members’ income and spending throughout the week, automatically finding savings. On average, Albert members save more than $450 per year.

Investing: Albert offers custom portfolios tailored to a member’s goals and time horizon and individual stocks and stock collections. All investments have just a $1 minimum, and all trades are commission-free.

Albert Genius: For a pay-what-is-fair monthly fee (minimum $4/month), Albert members have unlimited access to Albert’s financial professionals and a customized financial plan. Albert Genius answers any financial question, ranging from how to pay down debt faster to buying versus leasing a car to something as simple as making room for coffee in your budget.

“Everyone Deserves Access to Expert, Honest Advice”

“High-quality personalized financial advice has always been reserved for very few people. But without good advice, even the best financial tools can fail to deliver great financial outcomes,” said Yinon Ravid, CEO of Albert, about the service. “We believe that everyone deserves access to expert, honest money advice, regardless of income or net worth. Providing that advice alongside amazing financial products positions Albert as the all-in-one financial app for the next generation.”

Choosing a debit card can be challenging. There are dozens of new checking accounts popping up every month, all offering new features or perks designed to attract new accounts.

Both Extra Mastercard and Aspiration enjoy popularity among Americans conscious about their spending. The latter because they are conscious of the environment and their impact on it, and the latter are concerned about boosting their credit without a credit check. But both cards provide significant value not normally found outside of a credit card – but which is right for you?

Before you get your next debit or credit card, check out this helpful guide that breaks down both cards, their strengths, weaknesses, and the finer points that can help you make an informed decision.

How Popular are Debit Cards?

According to research from the Federal Reserve, 97% of U.S. consumers had a payment card of some variety. Of that proportion with a payment card, 85% had a debit card. Additionally, 68% of consumers used a debit card each month, compared to 74% using cash, and 63% using credit cards.

The same study found that debit cards still make up a significant proportion of how payments are made. Here is how consumers split their spending between payment types:

Debit

Credit

Cash

Other

38%

30%

23%

9%

So despite the allure of credit cards, there appears to remain a strong demand for debit cards amongst the American public. According to Statista, more than 270 million Mastercard debit cards are currently in circulation in the U.S. alone. Even more mind-boggling, there are roughly 2.5 billion (yes, billion) Visa debit cards worldwide.

Extra Mastercard or Aspiration Card: Which Is Right for You?

Before you decide on your next debit card, check out how both accounts break down:

How to Get the Debit Card

Here is all the information you’ll need to apply for both debit cards:

What Information Do You Need to Open an Extra Mastercard Account?

Name

Address

Email address

Phone number

SSN (for verification purposes)

External bank account information (account number and routing number)

What Information Do You Need to Open an Aspiration Spend & Save or Plus Account?

Name

Address

Email address

Phone number

SSN (for identification/verification purposes)

External bank account information for funding account (account number and routing number)

Does the Card Build Credit?

Aspiration’s debit card does not build credit (although the Aspiration Zero Mastercard does). The Extra Mastercard, on the other hand, is a debit card that builds credit – without a credit check.

The Extra credit builder process works by signing up and linking your bank account to Extra. Extra requires your bank to be Plaid compatible – but this won’t be an issue for most. Plaid connects with over 10,000 banks, making Extra near-universal for those with a U.S. deposit account.

One connected, Extra will calculate your “spending power” based on your transaction history and bank account balance. This spending power is your daily spend limit with the Extra Mastercard. Extra automatically repays itself daily, so your spending power replenishes every 24 hours.

Every month, Extra reports your spending to the three major credit bureaus. This process helps you build credit. Your credit utilization will be reported as 0%, and your payment history will be perfect, thanks to Extra’s automatic repayment system.

Card Fees

Aspiration Fees

Aspiration Plus is the premium tier of Aspiration and provides far more than just cash back rewards:

Up to 5.00% APY on Aspiration savings accounts

One out-of-network ATM reimbursement monthly

Carbon offsets for all your gas purchases with Planet Protection

The carbon offset feature with Aspiration Plus is unique. The company automatically offsets the carbon dioxide from gas purchased with the eligible card through carbon offset programs – including the planting of trees.

Aspiration Plus costs $7.99 per month or $95.88 per year ($71.88 if paid upfront). If you opt for the free Aspiration account, you’ll earn up to 5% back on Conscience Coalition purchases but do not earn any interest on deposits.

Extra Fees

The debit card is ideal for anyone newer to credit that doesn’t want the negative impact of a hard credit inquiry but still wants to earn rewards and boost their score for as little as $7 per month.

That $7 monthly charge is payable as an $84 yearly lump sum. Alternatively, members can opt for the Extra Rewards plan, which provides access to rewards points on eligible purchases. Extra Rewards costs $12 per month or $108 when billed annually.

Is there a free option?

Yes. Aspiration’s basic account (including the debit card) is available for as low as $0. Aspiration commits to “All Extra Services Provided at Cost,” meaning that it will only charge you what it costs them to provide the extra service, with Plus being this additional cost.

There is no free version of the Extra Mastercard. That said, Extra operates as much more than a basic checking or debit account, so this is understandable.

Does the Account Earn Interest?

As noted above, Aspiration Plus offers up to 5% APY on savings accounts. This 5% APY applies only after cardholders use their Aspiration debit card to make at least $1,000 in purchases per month.

Basic Aspiration members can also earn interest on their savings. Spending $1,000 on purchases with the Aspiration debit Mastercard entitles the basic member to #% APY on Aspiration savings, for no monthly service fee.

Because Extra only links to your external bank account, it does not earn any interest on deposited funds.

Rewards

Aspiration

The Aspiration Debit Card lets users do their part in conservation while earning impressive cash back on eligible purchases simultaneously. Rewards with the Aspiration Card differ from Extra in that they place a premium on “conscious brands.”

Aspiration partners with the Conscience Coalition to help cardmembers earn rewards on brands actively helping the environment. Eligible companies (that Aspiration says are “doing the right thing” include names such as Warby Parker, TOMS, Blue Apron, and more.

Keep in mind that earning the highest tier rewards with Aspiration requires an active Aspiration Plus membership.

Extra

Extra Mastercard members can earn rewards provided they opt for the $12/month Extra Rewards + Credit Building plan. With the Extra Rewards program, cardmembers earn Extra reward points on every purchase, with points redeemable in the Extra Rewards portal. The rewards portal provides the typical array of redemption options you’d normally find with a reward program, including merchandise and gift cards.

Recap

Here is a quick recap of all the features of both cards:

Extra Mastercard

Every purchase builds your credit. At the end of every month, purchases made with the Extra Debit Card are tallied up and reported to credit bureaus

0% interest

Connects with your bank account

Earn up to 1% in points for everyday purchases like rideshares, coffees, and your phone bills

Plans start at $7/month (based on an annual subscription)

Citi and Sears are joining forces for a new acquisition bonus for the popular Shop Your Way Mastercard®. Through January 20223, new cardmembers can earn a $75 statement credit every time they spend $500 with their card – up to $225 in credits. Here’s everything you need to know about Citi’s latest sign-up bonus for the Shop Your Way credit card:

Earn up to $225 Back in Statement Credits

Consumers with a rewards card in their wallet use those rewards to treat themselves and make purchases they wouldn’t normally make. That is the biggest finding of a 2021 Citi survey with The Harris Poll. To help attract new cardmembers, Citi is offering a lucrative Shop Your Way Mastercard® sign-up bonus.

Beginning May 8, 2022, newly-approved Shop Your Way Mastercard cardmembers can earn a $75 statement credit for every $500 spent, up to $225, on eligible purchases made within their first 90 days with the card. The statement credits will be automatically applied and credited to the account within eight weeks after the 90-day window. This offer is available for new cardmembers until January 28, 2023.

About the Shop Your Way Mastercard

Shop Your Way Mastercard cardmembers earn Shop Your Way Global Points on everyday purchases, including:

5% back on qualifying gas station purchases. This doesn’t include gas available at superstores or warehouse clubs

3% back on qualifying restaurants, including fast food places, bars, and cafes. This doesn’t include restaurants located inside another store

3% back on qualifying grocery store purchases. This doesn’t include superstores, warehouse clubs, or convenience stores

2% back on Sears and Kmart purchases made in-store*

Global Points earned with the Citi Shop Your Way Sears credit card are redeemable for gift cards on the Shop Your Way website or the Shop Your Way MAX App. Points are also redeemable for immediate savings on purchases at Sears, Sears Hometown Stores, and their online platforms. Available gift cards include options for hundreds of popular brands, including Airbnb, Sephora, Uber, and Walmart.

Family life may look different for everyone, from soccer games and ballet recitals to family dinners and other everyday necessities. One thing is for sure: a family should be taken care of, and having the right credit card can help better manage expenses to meet their needs. Here are our picks for the best family credit cards:

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

American ExpressProcessing Network

$0 for the first year. Then $95Annual Fee

Blue Cash Preferred® Card from American Express

19.24% to 29.99% variable based on creditworthiness the Prime RateRegular Purchase APR

19.24% to 29.99% variable based on creditworthiness the Prime RateBalance Transfer APR

29.99% variable based on the Prime RateCash Advance APR

0% for 12 months from account opening dateIntro Purchase APR

At a

Glance

Through the Blue Cash Preferred® Card from American Express, you can earn sizable cash back rewards on purchases in common categories, including 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1%), 3% cash back at U.S. gas stations and select U.S. department stores, and 1% on all other purchases. You can also earn $300 back in the form of a statement credit after you make $3,000 in purchases using your new card in the first six months of the account being open.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn a $300 statement credit after you spend $3,000 in purchases on your new Card within the first 6 months.

$0 intro annual fee for the first year, then $95.

Buy Now, Pay Later: Enjoy $0 intro plan fees when you use Plan It® to split up large purchases into monthly installments. Pay $0 intro plan fees on plans created during the first 12 months from the date of account opening. Plans created after that will have a monthly plan fee up to 1.33% of each eligible purchase amount moved into a plan based on the plan duration, the APR that would otherwise apply to the purchase, and other factors.

Low Intro APR: 0% on purchases and balance transfers for 12 months from the date of account opening. After that, your APR will be a variable APR of 19.24% – 29.99%. Variable APRs will not exceed 29.99%.

6% Cash Back at U.S. supermarkets on up to $6,000 per year in purchases (then 1%).

6% Cash Back on select U.S. streaming subscriptions.

3% Cash Back at U.S. gas stations and on transit (including taxis/rideshare, parking, tolls, trains, buses and more).

1% Cash Back on other purchases.

Cash Back is received in the form of Reward Dollars that can be redeemed as a statement credit

Get up to $120 in statement credits annually when you pay for an Equinox+ membership at equinoxplus.com with your Blue Cash Preferred® Card. That’s $10 in statement credits each month. Enrollment required.

Thinking about getting The Disney Bundle which includes Disney+, Hulu, and ESPN+? Your decision made easy with $7/month back in the form of a statement credit after you spend $12.99 or more each month on an eligible subscription with your Blue Cash Preferred Card. Enrollment required.

Terms Apply.

Intro Purchase APR:

0% for 12 months from account opening date

Regular Purchase APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Intro Balance Transfer APR:

0% for 12 months from account opening date

Balance Transfer APR:

19.24% to 29.99% variable based on creditworthiness the Prime Rate

Balance Transfer Transaction Fee:

Either $5 or 3% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.99% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Penalty APR:

29.99% variable based on the Prime Rate

Annual Fee:

$0 for the first year. Then $95

Foreign Transaction Fee:

2.7% of the transaction amount in U.S. dollars

Late Payment Penalty Fee:

Up to $40

Return Payment Penalty Fee:

Up to $40

You budget for family spending and want a credit card that earns significant cash back

You’ll spend a lot of money on groceries to take advantage 6% cash back at U.S. supermarkets on up to $6,000 in annual purchases (then 1% after that)

You’re excited at the prospect of earning 6% cash back with select streaming services

You want to capitalize on your commute with 3% cash back at U.S. gas stations (and select U.S. department stores)

You’ll take advantage of 3% cash back on transit (taxis/rideshare, parking and tolls, trains, buses and more), and 1% on all other purchases

You’re likely to make $3,000 in purchases within the first six months of the account opening to qualify for a one-time $300 statement credit

You cook at home often and commute to work and school regularly, or make use of public transit regularly

You must feed the family! Get dinner started with the Blue Cash Preferred® Card from American Express. With this card, you will earn 6% cash back (on the first $6,000 of eligible purchases) the next time you go grocery shopping. The same goes for streaming services from select providers, like Netflix or HBO Max, so don’t forget to buy some popcorn at the grocery store for your next family movie night.

The Blue Cash Preferred® Card from American Express has other ways to gain rewards, including 3% cash back at U.S gas stations and on transit, plus 1% cash back on other purchases. Your earned cash back is received as Reward Dollars which you can then redeem for statement credits. If you’re looking to apply for this card, you should also know new cardmembers can earn $350 back after spending $3,000 within six months of the account opening.

Furthermore, you can get exclusive access to entertainment tickets through American Express Experiences and enjoy taking your family out for some fun to the next ball game or whatever the next family event is. Another featured benefit is the annual $120 Equinox+ credit, which can help balance the yearly fee if you plan to use the health and fitness app. The also card features a $0 annual fee for the first year. After that you’ll pay $95 each year you remain a cardmember. If you’re not a fan of the annual fee, however, check out the Blue Cash Everyday® Card from American Express.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

$0Annual Fee

Citi Custom Cash℠ Card

18.99% – 28.99% (Variable)Regular Purchase APR

18.99% – 28.99% (Variable)Balance Transfer APR

29.99% (Variable)Cash Advance APR

0% for 15 months on PurchasesIntro Purchase APR

At a

Glance

The Citi Custom Cash? Card is a generous cash back credit card that offers up to 5% back on eligible purchases. The card, from Citi, does not charge an annual fee and rewards 5% back on the top spending category each month, with options including transit, travel, gas, groceries, dining, and more.

Best Benefits

Rates & Fees

Why Should You Apply?

Earn $200 cash back after you spend $1,500 on purchases in the first 6 months of account opening. This bonus offer will be fulfilled as 20,000 ThankYou® Points, which can be redeemed for $200 cash back.

0% Intro APR on balance transfers and purchases for 15 months. After that, the variable APR will be 18.99% – 28.99%, based on your creditworthiness.

Earn 5% cash back on purchases in your top eligible spend category each billing cycle, up to the first $500 spent, 1% cash back thereafter. Also, earn unlimited 1% cash back on all other purchases.

No rotating bonus categories to sign up for – as your spending changes each billing cycle, your earn adjusts automatically when you spend in any of the eligible categories.

No Annual Fee

Citi will only issue one Citi Custom Cash℠ Card account per person.

Intro Purchase APR:

0% for 15 months on Purchases

Regular Purchase APR:

18.99% – 28.99% (Variable)

Intro Balance Transfer APR:

0% for 15 months on Balance Transfers

Balance Transfer APR:

18.99% – 28.99% (Variable)

Balance Transfer Transaction Fee:

5% of each balance transfer; $5 minimum.

Cash Advance APR:

29.99% (Variable)

Cash Advance Transaction Fee:

5% of each cash advance; $10 minimum

Penalty APR:

Up to 29.99% (Variable)

Annual Fee:

$0

Foreign Transaction Fee:

3%

Late Payment Penalty Fee:

Up to $41

Return Payment Penalty Fee:

Up to $41

You want to earn 5% back but do’t want quarterly categories

You plan on spending $1,500 within the first 90 days

You have a large purchase in mind that you want to pay down over time

You plan on transferring an existing balance within the first four months

If your family spending changes from month to month, consider the Citi Custom Cash℠ Card. With this card you can earn 5% cash back on your top eligible spend category (up to $500 spent each billing cycle). There are 10 different eligible categories, ranging from grocery stores and restaurants to home improvement stores, live entertainment, and more.

In other words, you do not have to worry about keeping up with rotating categories or enrolling in them to earn rewards. Additionally, you can earn 1% unlimited cash back on all other purchases. Then, redeem your ThankYou® points with flexibility – as a statement credit, direct deposit, or check.

And if you are thinking of applying for the Citi Custom Cash℠ Card because it’s the right fit for your family’s needs, you will be happy to know there is a bonus offer. With the Citi Custom Cash℠ Card, you can earn $200 cash back after spending $750 in the first three months. To break it down into smaller numbers, making $250 worth in purchases each month (in the first three months) will earn you the $200 cash back bonus. Not too bad if you already spend that amount on something like groceries – or any of the eligible spend categories.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

VisaProcessing Network

NoneAnnual Fee

Prime Visa

18.74% to 26.74% variableRegular Purchase APR

18.74% to 26.74% variableBalance Transfer APR

29.49% variable based on the Prime RateCash Advance APR

At a

Glance

The Prime Visa offers cardholders impressive rewards on all Amazon.com and Whole Foods purchases, as well as elevated cash back at gas stations, drug stores, restaurants, transit, commuting, and more.

Best Benefits

Rates & Fees

Why Should You Apply?

Instant Amazon.com gift card on approval

Earn 5% Back at Amazon.com and Whole Foods Market with an eligible Prime membership, plus 5% Back on purchases made through Chase Travel.

Earn 2% Back at restaurants, gas stations, and drugstores, plus 2% Back on local transit and commuting, including rideshare.

Earn 1% Back on all other purchases

No foreign transaction fees

No annual fee

Regular Purchase APR:

18.74% to 26.74% variable

Intro Balance Transfer APR:

N/A

Balance Transfer APR:

18.74% to 26.74% variable

Balance Transfer Transaction Fee:

Either $5 or 5% of the amount of each transfer, whichever is greater

Cash Advance APR:

29.49% variable based on the Prime Rate

Cash Advance Transaction Fee:

Either $10 or 5% of the amount of each cash advance, whichever is greater

Late Payment Penalty Fee:

Up to $39

Return Payment Penalty Fee:

Up to $39

Minimum Deposit Required:

N/A

You frequently shop at Amazon or Whole Foods

You have an existing Amazon Prime membership

You want a card with no foreign transaction fees and Visa concierge services for your travel plans

You want a flexible rewards program, including savings at gas stations dining

You want the excellent customer service Amazon is known for

The Amazon Prime Rewards Visa Signature Card is for the family that takes online shopping to the next level. When Amazon.com is your go-to online shop, the Amazon Prime Rewards Visa Signature Card can go a long way. The credit card allows cardholders to earn 5% back when shopping on Amazon.com and at Whole Foods Market.

The best part is your rewards are not limited to online shopping. You can earn 2% back at restaurants, gas stations, and drugstores. This is a nice benefit to have when you want to treat the family out for dinner or need to take care of a handy drugstore purchase. In addition, you earn 1% back on all other purchases, wherever your shopping takes you.

A surprising feature of the Amazon Prime Rewards Visa Signature Card is it has no foreign transaction fees. This perk makes it an excellent credit card option to take on your next family vacation – especially if it’s abroad. And upon approval, you will instantly receive a $100 Amazon Gift Card Bonus.

A Prime membership is required for this credit card. However, if you don’t have a Prime membership, you could qualify for the Amazon Rewards Visa Card.

BestCards refers to a variation of FICO Score 9, which is one of many different types of credit scores. A financial institution may use a different score when deciding whether to approve you for a credit card. Please note that the range shown here is our own estimation and not a guarantee of credit needed to be approved for any given card.

Recommended Credit:Excellent / Good

MastercardProcessing Network

$0Annual Fee

Citi® Double Cash Card – 18 month BT offer

18.99% – 28.99% (Variable)Regular Purchase APR

18.99% – 28.99% (Variable)Balance Transfer APR

29.99% (Variable)Cash Advance APR

At a

Glance